Long story short: This beginner’s guide to Indian Motor Insurance Tariff (IMT) for two-wheelers in India will help you understand deductibles, add-ons, premiums, IMT 24, IMT 22A, exclusions, and more, so you can choose the right policy.

Have you ever seen the term IMT when you were a motorcycle owner? Most two-wheeler owners have not. You might have spotted it in your insurance documents. Usually, we print these papers, keep them with our bikes, or store them digitally. No worries—let’s talk about what Indian Motor Tariffs (IMT) for two-wheelers actually mean.

Motor insurance in India is governed by several Indian Motor Tariffs (IMTs), which offer different endorsements and coverage options. In this blog, we’ll focus on the main IMTs for two-wheelers, so you can understand their benefits and how they work. We won’t go through every IMT, since most people only need a few, but you’ll find a complete list in the table below.

Key Takeaways

- IMT Endorsements Shape Your Policy: Indian Motor Tariff (IMT) endorsements are official add-ons or modifications to your two-wheeler insurance policy, impacting coverage, premiums, and claims. Understanding which IMTs apply to your situation helps you choose the right protection.

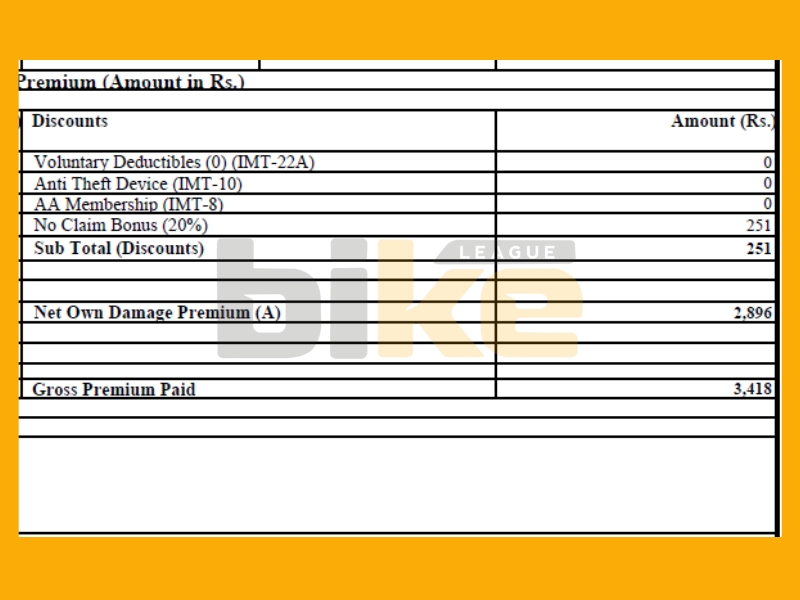

- Essential IMTs for Most Owners: IMT-22 (compulsory deductible) and IMT-15 (personal accident cover for owner-driver) are essential for almost every policyholder. IMT-22A (voluntary deductible), IMT-24 (accessory cover), and IMT-33 (loss of accessories) are useful options, depending on your needs and risk appetite.

- Discounts and Premium Reductions: Certain IMTs offer direct discounts on your own-damage premium—for example, IMT-10 for fitting an ARAI-approved anti-theft device, IMT-8 for automobile association membership, and IMT-12 for specially modified vehicles for disabled users. These can help lower your insurance costs if you qualify.

- Declare Accessories and Deductibles Clearly: Always declare any electrical/electronic accessories to ensure coverage (IMT-24/33). Know the difference between compulsory and voluntary deductibles: both affect your out-of-pocket payments during a claim, so check them on your policy schedule before buying or renewing.

- Check for Updates and Read the Fine Print: IMT rules, coverage, and premiums may change over time due to regulatory updates. Always check the latest official sources (IRDAI, your insurer’s website, and your policy schedule) for the most accurate and current information before making insurance decisions.

What Is Imt For Two-wheelers In India?

In the context of motor insurance in India, IMT stands for the Indian Motor Tariff. It is a set of guidelines issued by the Insurance Regulatory and Development Authority of India (IRDAI) that regulates the pricing and coverage of motor insurance policies, including two-wheeler policies. The IMT specifies endorsements, coverage options, and conditions for insurers to follow when offering motor insurance.

List Of All Imts Applicable To Two-wheelers In India

| IMT No. | Endorsement Title |

|---|---|

| IMT-1 | Extension of Geographical Area (beyond India) |

| IMT-3 | Automatic Transfer of Liability-Only Policies on Sale of the Vehicle |

| IMT-4 | Substitution of the Insured Vehicle (same-class replacement) |

| IMT-5 | Demonstration / Tuition Use (test-rides, rider training) |

| IMT-6 | Lease Agreement |

| IMT-7 | Vehicles Subject to Hypothecation Agreement |

| IMT-8 | Discount for Membership of Recognised Automobile Associations |

| IMT-11 | Termination of the Undeclared Laid-Up Period |

| IMT-12 | Discount for Specially Designed/Modified Vehicles (for person with a disability) |

| IMT-15 | Personal Accident Cover for Owner-Driver |

| IMT16 | Personal Accident Cover for Unnamed Passengers (up to seating capacity) |

| IMT-17 | Personal Accident Cover for Paid Driver/Cleaner |

| IMT-18 | Personal Accident Cover for Hirer/Driver (if used on hire/reward) |

| IMT-20 | Reduction in Limit of Liability for Third-Party Property Damage |

| IMT-22 | Compulsory Deductible (fixed amount per claim) |

| IMT-22A | Voluntary Deductible (higher deductible in exchange for lower premium) |

| IMT-24 | Electrical / Electronic Fittings (to cover battery, controller, lights, etc.) |

| IMT-25 | CNG/LPG Kit in Bi-Fuel System (own-damage cover for the kit; analogous for alternate-fuel EVs) |

| IMT-32 | Accidents to Soldiers/Sailors/Airmen Employed as Drivers |

| IMT-33 | Loss of Accessories (theft or damage to rider’s accessories) |

| IMT-35 | Hired Vehicle – Driven by Hirer (two-wheelers on hiring contracts) |

As mentioned earlier, we won’t cover every Indian Motor Tariff for two-wheelers. Let’s now look more closely at some of the main IMTs for two-wheelers.

1. Imt-1: Extended Geographical Area Coverage

Scope Of Cover

IMT-1 allows the insured two-wheeler to be legally used in neighbouring countries, with insurance cover extended to:

- Bangladesh

- Bhutan

- Nepal

- Pakistan

- Sri Lanka

- Maldives

The regular comprehensive (own-damage and third-party) or third-party-only cover remains valid in these countries during the policy period.

Premium Calculation

- Comprehensive Policy (Own-Damage + TP): Additional premium of ₹500 per year.

- Third-Party-Only Policy: Additional premium of ₹100 per year.

- This flat fee is not dependent on the IDV or cubic capacity.

Exclusions & Limits

- No coverage during sea or air transit to the extended countries.

- Only valid in the listed countries (other countries not allowed).

- All standard exclusions and limitations of the base policy still apply.

Practical Example

Raj plans a road trip from Siliguri to Bhutan on his Royal Enfield bike. His Indian insurance doesn’t cover Bhutan unless IMT-1 is added.

For an additional premium of ₹500, Raj gets complete insurance protection in Bhutan. However, if he were to ferry the bike by sea or air, any damage in transit would not be covered.

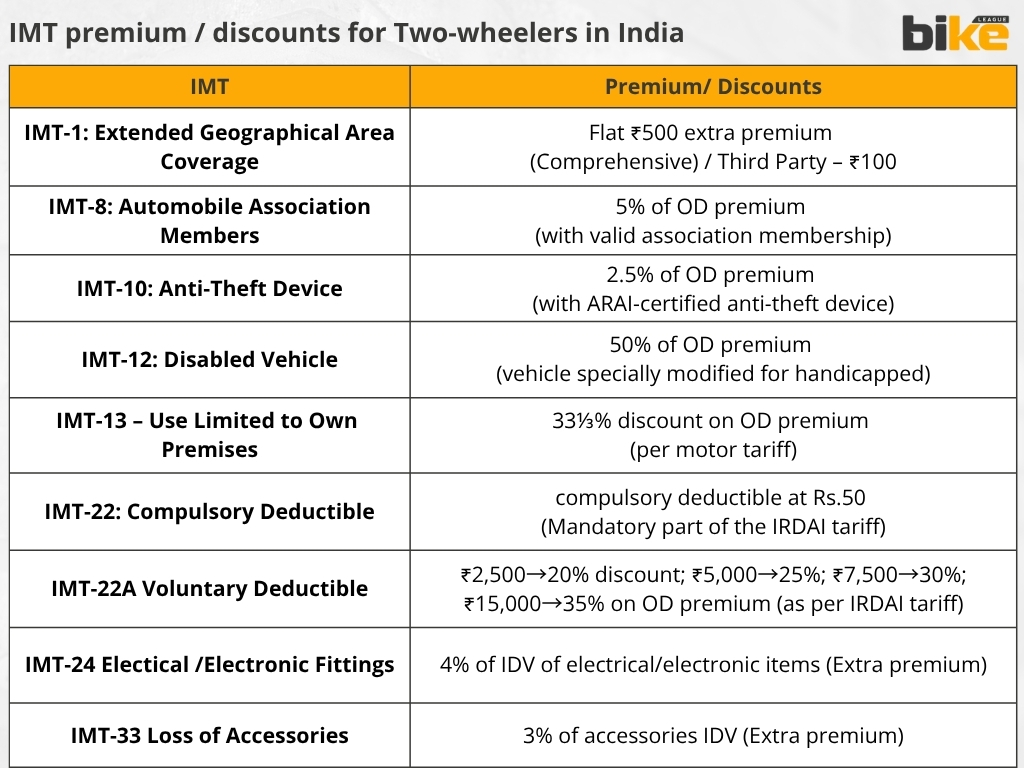

| Insurer | IMT-1: Extended Geographical Area Coverage |

|---|---|

| All insurers | Flat ₹500 extra premium (Comprehensive) / Third Party – ₹100 |

2. Imt-8: Automobile Association Members

Scope Of Cover

This endorsement provides a discount on the own-damage portion of the premium for two-wheeler owners who are members of a recognised automobile association, such as:

Recognised Associations

Membership in any one association below qualifies for IMT-8; multiple enrollments do not stack:

- Automobile Association of Eastern India (AAEI)

- Uttar Pradesh Automobile Association (UPAA)

- Western India Automobile Association (WIAA)

- Automobile Association of Southern India (AASI)

- Automobile Association of Upper India (AAUI)

Premium Calculation

- Discount: 5% of the Own-Damage premium

- Maximum cap: ₹50 per year

- Discount applies only to the OD portion, not the TP premium.

- The discount is adjusted pro rata if the policy is taken mid-membership or membership lapses mid-policy.

Exclusions & Limits

- Membership must be active and from a recognised association.

- Only one discount is allowed per policy.

- If membership ends early, the insurer must refund the unutilised discount.

- No effect in third-party-only policies (no discount applicable).

Practical Example

Sita rides a Honda Activa and has a yearly OD premium of ₹1,000. As a member of the Automobile Association of Southern India, she is eligible for a 5% discount.

That’s ₹50 (maximum cap), reducing her OD premium to ₹950. If she leaves the association after 6 months, she must return the unutilised portion of the discount, i.e., ₹ 25.

| Insurer | IMT-8: Automobile Association Members |

|---|---|

| All insurers | 5% of OD premium (with valid automobile-association membership) |

3. Imt-10: Anti-theft Device

Scope Of Cover

Under IMT-10, if you install an ARAI-approved anti-theft device (like a GPS tracker or alarm) on your motorcycle or scooter and get it certified by a recognised automobile association, you become eligible for a tariff discount on the policy. The insurance policy will be endorsed to note that your vehicle has this device.

This endorsement does not change your coverage; it acknowledges the device and gives you a premium break. (It’s not applicable for motor-trade policies where the vehicle is under repair or being sold.)

Premium Calculation

The Indian Motor Tariff provides a 2.5% discount on the own-damage premium, up to a maximum of ₹500. In practice, insurers cap the discount (often around ₹200–₹500, depending on the company) even if 2.5% of your premium exceeds that.

The discount applies to the own-damage (OD) portion of the premium. For example, if your OD premium is ₹10,000, a 2.5% discount would be ₹250 (within the ₹500 cap). If you install the device mid-policy, the insurer provides a pro rata discount for the remaining period. These discounts are standardised across insurers by the tariff.

Exclusions & Limits

- Maintenance of Anti-Theft Device: Must be kept in good working order for the duration of the policy to retain benefits.

- Removal or Disabling: If the device is removed or disabled, the insurer may withdraw the discount.

- Certification Requirement: The anti-theft device must be certified by ARAI at the time of policy issuance or added later.

- Premium Implications: IMT-10 affects premium rates but does not automatically provide theft coverage.

- Vehicle Type Limitation: Discount applies only to two-wheelers classified as private vehicles (not for commercial use such as taxis, bikes for hire, or motor-trade).

- Commercial Use Exemption: Different rules apply if the bike is used for hire or commerce; IMT-10 is not applicable for motor trade policies.

Practical Example

Ramesh owns a scooter and adds a certified anti-theft tracker before renewal. His OD premium is ₹4,000. Under IMT-10, he gets 2.5% off, i.e. ₹100 (since 2.5% of 4,000 = 100).

Thus, his payable OD premium becomes ₹3,900 (plus any mandatory third-party premium). If Ramesh installed the device halfway through the year, he’d get roughly half of that ₹100 as a pro-rated discount.

For more in-depth details, you can check our detailed article about the same here Best anti-theft devices for bikes: Secure your ride today

| Insurer | IMT-10: Anti-Theft Device |

|---|---|

| All insurers | 2.5% of OD premium (with ARAI-certified anti-theft device) |

4. Imt-12: Disabled Vehicle

Scope Of Cover

IMT-12 applies when the insured two-wheeler is specifically built or modified for a blind, disabled, or mentally challenged person. In India, the regional transport office officially endorses such vehicles in the vehicle’s registration book.

If your bike or scooter has this special status, the insurer adds IMT-12 to the policy. This endorsement recognises the vehicle’s exceptional design and grants you a significant discount. Again, IMT-12 does not provide additional coverage beyond the regular policy terms; it merely lowers the premium.

Premium Calculation

The tariff provides a 50% discount on the own-damage premium for vehicles under IMT-12. For instance, if the OD premium for such a bike is usually ₹6,000, you only pay ₹3,000. This is a straight half-price on the OD part.

No separate cap is mentioned in the tariff for this endorsement (the discount is half, regardless of premium). Note that this discount applies only to the OD portion, so your third-party premium (set by government rates) remains unaffected.

Exclusions & Limits

- IMT-12 discounts insurance premiums for bikes registered as specially designed for disabled persons.

- Official endorsement must be present on the registration certificate for the discount to apply.

- If modifications are removed or the insured no longer qualifies, the insurer can cancel the discount.

- The discount applies only to private non-commercial vehicles.

- Commercial vehicles, such as ambulances or taxis, are not eligible for the discount.

- IMT-12 does not change liability coverage.

Practical Example

Geeta has a three-wheeler scooter specially fitted with hand controls for her quadriplegic father. It’s legally registered as a “vehicle for disabled people.” Her insurer applied IMT-12, cutting her OD premium from ₹8,000 to ₹4,000 (50% off).

So, she pays ₹4,000 plus the third-party charge. Suppose she loses the special registration or no longer fits the criteria. In that case, the insurer will remove IMT-12 on renewal and charge the full premium.

| Insurer | IMT-12: Disabled Vehicle |

|---|---|

| All insurers | 50% of OD premium (vehicle specially modified for blind/handicapped) |

5. Imt-13: Use Limited To Own Premises

Scope Of Cover

The policy covers loss or damage only when the vehicle is used on the insured’s own premises, meaning private property that isn’t open to the public. If the vehicle is used elsewhere, it isn’t covered. The only exception is if the vehicle is used to fight a fire, which is still covered. “Own premises” means areas where the public does not have general access.

In practice, the insurer pays only for accidents or theft on the owner’s property; incidents on public roads or elsewhere are not covered.

Premium Calculation

Since there’s no risk from using the bike on public roads, insurers usually lower the premium when IMT-13 is added. While there’s no fixed rate from IRDAI, insurers often give about a 33% discount on the own-damage premium, as per the motor tariff.

The own-damage part of the premium is often much lower when the vehicle stays on private property, since the risk is less. The exact discount depends on the insurer, because IRDAI does not set a specific percentage.

Exclusions And Limits

- Besides the standard policy exclusions (e.g., mechanical breakdown, wear and tear), IMT-13 explicitly excludes use outside the insured’s premises.

- If the bike is ridden on a public road or any area with public access, this endorsement does not cover any resulting damage/injury.

- IMT-13 does not add separate exclusions (beyond the above and normal policy exceptions).

Limits Of Liability

The sum insured (IDV) and third-party limits remain per the base policy. Still, they effectively apply only on the premises. For example, suppose a third party is injured on the insured property. In that case, the insurer pays up to the policy limit (subject to usual legal limits).

However, no liability applies off-premises. In short, the insurer’s maximum payment (IDV or third-party limit) is unchanged but is enforceable only for on-premises incidents.

Practical Example

A two-wheeler owner who only drives on his private farm might purchase IMT-13. Suppose the bike slips on the farm and damages itself (or injures someone on the farm). In that case, the insurer pays per the IDV or liability limit.

| Insurer | IMT-13 – Use Limited to Own Premises |

|---|---|

| All insurers | 33⅓% discount on OD premium (per motor tariff) |

However, if the same bike is taken onto a public road, any accident there won’t be covered by this endorsement. IMT-13 is best for vehicles that always stay on private property, and insurers offer a lower premium for this limited use.

6. Imt-15 personal Accident Cover For Owner-driver

Scope Of Cover

When you hold IMT 15 on your two-wheeler, the policy pays out a lump sum—based on the CSI—if the owner-driver suffers bodily injury or death directly due to an accident involving the insured bike (including mounting into/dismounting from it)

Premium Calculation

IRDAI has prescribed a flat rate of ₹50 per ₹1 lakh of CSI per year. With the mandatory CSI now ₹15 lakh, your annual premium (before GST) is:

₹50 × 15 (lakhs) = ₹750 per year

Exclusions & Limits

- Driving under the influence of alcohol or drugs

- Non-vehicular accidents (e.g., slipping at home)

- Intentional self-injury or suicide attempts

- War, invasion, riot, nuclear risks

Practical Example

Death Benefit

Mr X is fatally injured in a bike crash on May 8, 2025.

CSI: ₹15 lakh → Payout: 100% of CSI = ₹15 lakh.

Loss Of One Limb

Ms Y lost her left leg in a collision on April 22, 2025.

CSI: ₹15 lakh → Payout: 50% of CSI = ₹7.5 lakh.

Permanent Total Disablement

Mr Z suffered quadriplegia (complete paralysis) in an accident on March 30, 2025.

CSI: ₹15 lakh → Payout: 100% of CSI = ₹15 lakh.

| Nature of Injury | % of CSI Payable |

|---|---|

| Death | 100% |

| Loss of two limbs, or sight of both eyes, or one limb and one eye | 100% |

| Loss of one limb or sight of one eye | 50% |

| Permanent total disablement (other than above) | 100% |

7. Imt-16 personal Accident Cover For Unnamed Passengers

Scope Of Cover

When IMT 16 is taken, the insurer undertakes to pay compensation for bodily injury or death sustained by any unnamed passenger (other than the owner-driver, paid driver or cleaner) while mounting into, dismounting from, or travelling on the insured two-wheeler, caused by violent, accidental, external and visible means. The scale of compensation is:

| Nature of Injury | % of CSI Payable |

|---|---|

| Death | 100% |

| Loss of two limbs, or sight of both eyes, or one limb and one eye | 100% |

| Loss of one limb or sight of one eye | 50% |

| Permanent total disablement (other than above) | 100% |

Here, “CSI” refers to the Capital Sum Insured per passenger (inserted at policy inception).

Premium Calculation

IRDAI’s Motor Tariff specifies that the additional premium for IMT 16 on a private two-wheeler is ₹50 per passenger per annum (for a CSI of ₹1 lakh). You can align this with your policy’s term (1, 2, or 3 years), as multi-year terms are allowed under long-term third-party norms.

Exclusions & Limits

While IMT 16 broadens protection, the following standard exclusions apply (mirroring those under IMT 15 and general PA covers):

- Intoxication: No cover if the passenger is under the influence of alcohol or drugs at the time of the accident.

- Self-harm: Injuries or death due to intentional self-injury or suicide attempts.

- Non-vehicular incidents: Accidents not involving the insured two-wheeler (e.g., a fall at home).

- War & nuclear risks: Any injury arising from warlike operations, invasion, civil war, or nuclear radiation.

Additionally, total liability under IMT 16 per passenger per insurance period cannot exceed the chosen CSI for that passenger.

Practical Example

Death Of A Pillion Rider

Scenario: On May 5, 2025, Ms A meets with a fatal accident while riding pillion.

CSI: ₹1,00,000 → Payout: 100% of CSI = ₹1,00,000 to her nominee.

Loss Of One Limb

Scenario: On April 18, 2025, Mr B loses his left leg in a collision while riding pillion.

CSI: ₹1,00,000 → Payout: 50% of CSI = ₹50,000 to Mr. B.

Permanent Total Disablement

Scenario: On March 12, 2025, Mr C suffers complete paraplegia in an accident as an unnamed passenger.

CSI: ₹1,00,000 → Payout: 100% of CSI = ₹1,00,000 to Mr. C.

8. Imt-20 reduction In Limit Of Liability For Third-party Property Damage

Scope Of Cover

When you attach IMT-20 to your two-wheeler policy:

- Insurer’s liability for third-party property damage (i.e., damage to vehicles or property belonging to others) is capped at ₹6,000 per event.

- All other aspects of your third-party cover (bodily injury, death, legal defence costs) remain unchanged.

Premium Impact

IRDAI’s Motor Tariff specifies a flat ₹50 per annum premium reduction (pre-GST) for two-wheelers that opt for IMT 20. You can choose this for 1-, 2-, or 3-year third-party cover

Exclusion & Limits

Attaching IMT 20 only affects your insurer’s maximum payout for third-party property damage. All other exclusions of a standard two-wheeler third-party policy continue to apply.

Practical Examples

Minor Fender-bender

- Scenario: You clip a parked scooter, causing ₹4,000 of damage.

- Without IMT 20: Insurer pays full ₹4,000.

- With IMT 20: Insurer still pays ₹4,000 (under the ₹6,000 cap).

Moderate Collision

- Scenario: You collide with a car, rendering property damage of ₹8,500.

- Without IMT 20: Insurer pays full ₹8,500.

- With IMT 20: Insurer pays only ₹6,000; you’re responsible for the remaining ₹2,500 out-of-pocket.

Major Pile-up

- Scenario: A multi-vehicle accident causes ₹15,000 in third-party property damage.

- Without IMT 20: Insurer pays the full ₹15,000.

- With IMT 20: Insurer’s liability maxes out at ₹6,000; you must cover ₹9,000 yourself.

9. Imt-22: Compulsory Deductible

Scope Of Cover

Under IMT-22, the insured must pay a fixed portion of every Own Damage claim. IRDAI fixes this compulsory deductible for two-wheelers at Rs. 50. This means that in every claim (even total loss), the insured bears the first ₹50 of damage. The insurer pays the remainder (subject to the policy limit).

IMT-22 is mandatory per IRDAI rules for all two-wheeler comprehensive policies. It does not affect liability (third-party) coverage.

Premium Calculation

IMT-22 usually does not change the premium (it is a mandatory part of the IRDAI tariff). The standard tariff tables for two-wheelers assume this ₹50 deductible, so no additional premium is charged for adding IMT-22.

In other words, you don’t pay extra for IMT-22, but you also don’t get a discount for accepting it – it simply reduces the insurer’s payout per claim. (IRDAI’s General Rule GR.40 sets this deductible amount).

Exclusions And Limits

No notable exclusions are added by IMT-22 beyond those already present.

The only effect is that the insurer will not cover the first ₹50 of any own damage loss. All other policy terms apply as usual. For example, if the policy excludes wear and tear, that still applies.

But accident damage is covered above the deductible. Section II (third-party liability) is unaffected by IMT-22; it does not impose any deductible on liability claims (only on section I own damage claims).

Limits Of Liability

The policy’s declared value and third-party liability limits are unchanged. IMT-22 merely shifts the first Rs. 50 of each claim to the insured. For instance, if the vehicle’s IDV is ₹50,000 and it suffers ₹10,000 damage, the maximum insurer payout is ₹9,950 (₹10,000 – ₹50).

The insurer’s overall liability remains subject to the IDV and legal limits; IMT-22 only carves out that fixed ₹50 per claim.

Practical Example

Suppose a bike is damaged in an accident, and the repair estimate is ₹4,500. Under IMT-22, the owner pays ₹50 out of pocket; the insurer covers the remaining ₹4,450. If the damage had been ₹40,000, the insured would still pay ₹50, and the insurer would pay ₹ 39,950. The IMT-22 slightly reduces payouts per claim but has a negligible effect on premiums.

10. Imt-22a: Voluntary Deductible

Scope

Under IRDAI’s motor tariff, IMT 22A allows the policyholder to voluntarily accept an extra deductible (excess) on top of the compulsory deductible (₹100 for two wheelers.

The rider pays a fixed out-of-pocket amount per claim for a lower damage premium. The IRDAI endorsement wording specifies: “the insured, having opted for a voluntary deductible of Rs. X, a reduction in the premium of Rs. is allowed. Y under Section I of the policy… the insured shall bear … the first Rs. X (or any lesser expenditure) of any expenditure for which provision has been made under this policy”.

In other words, the rider pays the chosen amount per claim (including if the bike is a total loss), and the insurer pays the remainder up to the insured’s IDV.

Premium Rates

All IRDAI-approved insurers apply the standard tariff discount schedule. Typically, the discounts on Own Damage (OD) premium are:

- ₹2,500 deductible ⇒ 20% discount (max ₹750)

- ₹5,000 ⇒ 25% (max ₹1,500)

- ₹7,500 ⇒ 30% (max ₹2,000)

- ₹15,000 ⇒ 35% (max ₹2,500)

Exclusions

IMT 22A is not a coverage add-on but a premium modifier, so it has no notable exclusions beyond the standard policy terms. It applies only to Own Damage claims – third party liability and personal accident sections are unaffected. Importantly, the voluntary deductible is in addition to the compulsory ₹100 deductible on two-wheelers.

In a claim, both deductibles are applied. (E.g., with ₹5,000 voluntary plus ₹100 compulsory, the rider pays ₹5,100 per claim.) There is no IRDAI exclusion specific to voluntary deductibles; the rider bears that cost for any damage covered under Section I.

Limit Of Liability

There is no separate sum insured for IMT 22A; the “limit” is the deductible. The insured must pay the chosen amount each time. IRDAI’s tariff typically allows voluntary deductibles of up to ₹15,000 on two-wheelers.

In practice, insurers cap the maximum deductible and discount, as shown in the table below. The insurer’s liability is the loss minus the deductible (subject to the vehicle IDV and other limits).

Practical Example

A rider insures a motorcycle with an OD premium of ₹4,500. By selecting a ₹5,000 voluntary deductible, they earn a 25% discount (up to ₹1,500).

Suppose the discounted OD premium becomes ₹3,000. Later, the bike suffered ₹12,000 damage in an accident. The rider must pay ₹5,100 of that (₹5,000 voluntary + ₹100 compulsory), and the insurer covers the remaining ₹6,900 (subject to depreciation limits).

If the bike were a total loss (IDV ₹50,000), the rider would pay ₹5,100, and the insurer would pay ₹44,900.

| Insurer | IMT-22A Voluntary Deductible |

|---|---|

| All insurers | ₹2,500→20% discount; ₹5,000→25%; ₹7,500→30%; ₹15,000→35% on OD premium (as per IRDAI tariff) |

11. Imt-24: Electrical/electronic Fittings Cover

Scope

IMT 24 is an optional add-on that covers loss or damage to electrical/electronic accessories fitted to the bike (but not included in the manufacturer’s listed price). Examples include aftermarket items such as GPS units, sound systems, fog lamps, and charging ports.

The endorsement states that the insurer will indemnify the insured for any loss/damage to the specified electronic/electrical fittings (named in the policy schedule) caused by any insured perils (accident, fire, theft, etc.).

Note: Damage from mechanical failure or breakdown of the fittings is expressly excluded.

Premium Calculation

IRDAI’s tariff (G.R. 41) mandates an extra premium of 4% of the declared value of the electrical/electronic items. In practice, the insurer requires the rider to declare the total value of such accessories when purchasing IMT 24; the premium is simply 4% of that amount.

For example, if a motorcycle has a Bluetooth stereo system worth ₹10,000 fitted, the IMT 24 premium would be ₹400. (United India and other insurers confirm the 4% rule on their websites.)

Exclusions

- Per the endorsement, mechanical or electrical breakdown of the fittings is not covered.

- Only items listed in the schedule (whose value is declared) are insured.

- Damage to any non-declared accessory would not be payable.

- Otherwise, coverage follows the standard Section I perils. (Liability to third parties is unaffected by IMT 24, as this endorsement only extends the own damage cover to accessories.)

Limits Of Liability

The insurer’s maximum payout for any covered accessory loss is the Declared Value (IDV) entered in the policy.

In other words, if the rider declares an accessory’s value as ₹5,000, that is the cap on recovery for that item under IMT 24. Depreciation rules for parts generally apply to repair estimates as usual (except for a total loss where IDV is paid).

Practical Example

A rider adds an LED lamp and a mobile charger to their bike, worth ₹5,000. They buy an IMT 24 cover and pay an extra premium of 4% on ₹5,000 = ₹200. Later, these accessories are damaged in a covered collision.

The insurer will reimburse up to ₹5,000 (minus any salvage), subject to standard depreciation rules for repair parts. If the accessories had cost only ₹2,000, the extra premium would have been just ₹80, and the payout would have been capped at ₹2,000.

| Insurer | IMT-24 Electrical/Electronic Fittings |

|---|---|

| All insurers | 4% of IDV of electrical/electronic items (Extra premium) |

12. Imt-33: Loss Of Accessories Cover

Scope

This endorsement (IMT‐33) covers loss or damage to declared accessories (electrical or non-electrical) caused only by theft, burglary or housebreaking – provided the vehicle is not stolen in the same event.

It must be specifically purchased (payment of an additional premium). The insured must declare all accessories covered; then, the loss/theft of those items is indemnified.

Premium Calculation

Insurers typically charge an additional 3% premium on the total declared IDV of accessories. For example, United India Insurance explicitly notes that accessories cover (for bikes) is “covered on payment of an additional premium of 3% of the IDV of such accessories.”

Exclusions

- IMT-33 covers theft/burglary only. Any accidental damage to accessories (even in a crash) is not covered under this endorsement.

- Only loss by unauthorised taking is insured.

- All usual policy exclusions (e.g. wear-and-tear, mechanical breakdown) still apply otherwise.

Limit Of Liability

The claim payout is limited to the declared IDV of each accessory. If multiple items are covered, the insurer pays up to each item’s sum insured (aggregate not exceeding total declared accessories IDV).

Practical Example

A rider declares accessories (seat cover, bike cover, etc.) worth ₹10,000 and pays an extra premium of 3% × ₹10,000 = ₹300.

Suppose the helmet lock and cover (total IDV ₹2,000) are stolen. In that case, the insurer reimburses up to ₹2,000 (subject to depreciation) under this cover.

| Insurer | IMT-33 Loss of Accessories |

|---|---|

| All insurers | 3% of accessories IDV (Extra premium) |

Which Imts Are Essential, Optional, Or Rarely Used For The Average Two-wheeler Policyholder?

For most private two-wheeler owners, only a handful of IMTs are relevant in day-to-day use. IMT-22 is included in standard own-damage policies, while IMT-15 is the key personal accident cover. The remaining IMTs are generally optional or apply to specific situations.

| IMT | Use level | Best for | Notes |

|---|---|---|---|

| IMT-22 | Essential | Anyone buying comprehensive two-wheeler insurance | Compulsory deductible applies to own-damage claims. |

| IMT-15 | Essential | Owner-drivers | Personal accident cover for the owner-driver is the key cover most riders should know about. |

| IMT-22A | Optional | Riders willing to take higher out-of-pocket risk for lower premium | Voluntary deductible; useful only if you understand the claim trade-off. |

| IMT-24 | Optional | Owners with declared electrical/electronic accessories | Useful for expensive add-ons like chargers, lights, or controllers. |

| IMT-33 | Optional | Riders with declared accessories they want insured against theft | Narrow cover, mainly for theft/burglary/housebreaking, not accidental damage. |

| IMT-8 | Optional | Association members | Small premium discount if you are a recognised automobile association member. |

| IMT-10 | Optional | Riders using approved anti-theft devices | Discount-based endorsement, not a separate theft cover. |

| IMT-1 | Rarely used | Riders crossing into neighbouring countries | Relevant only for cross-border travel; not useful for normal city or highway use. |

| IMT-12 | Rarely used | Specially modified vehicles for disabled persons | Niche tariff benefit, not common for average riders. |

| IMT-13 | Rarely used | Vehicles used only on private premises | Only makes sense if the bike never goes on public roads. |

| IMT-16 | Rarely used | Policies that include unnamed passenger PA cover | More relevant for specific policy structures than for a typical solo rider. |

| IMT-20 | Rarely used | Riders intentionally reducing TP property-damage liability | Not a mainstream choice for private two-wheelers. |

| IMT-25, IMT-32, IMT-35 | Rarely used | Special fuel, employment, or hire-related cases | Mostly niche or commercial-use situations. |

In summary, most policyholders only need to be familiar with IMT-15, IMT-22, IMT-22A, IMT-24, and IMT-33. Other IMTs are relevant mainly for special cases like international travel, association membership, anti-theft devices, or modified vehicles.

For most people who own a commuter scooter or motorcycle, the main decisions are the standard compulsory deductible, choosing a voluntary deductible to save on premiums, and deciding whether to include accessories in your coverage.

To sum up, most riders should focus on IMT-15 and IMT-22. IMT-8, IMT-10, IMT-22A, IMT-24, and IMT-33 are optional, and the others are mainly for special cases.

How Imts Or Tariffs May Change Over Time, Or Where To Check For Updates In India?

Indian Motor Tariff provisions and IMT-related policy terms may change over time due to regulatory updates, revised insurer wording, product changes, or updated underwriting practices. That means an older article, policy copy, or endorsement schedule may not always reflect the latest version available to policyholders. To stay updated, readers should always verify the latest wording through official regulatory and insurer sources before relying on any tariff reference or premium illustration.

| Source | What to check there | Official link |

|---|---|---|

| IRDAI | Regulations, circulars, master circulars, guidelines, and official insurance-related notifications | https://irdai.gov.in/ |

| IRDAI notifications / circulars section | Latest regulatory announcements, circulars, compliance updates, and official changes affecting insurers or policyholders | IRDAI document / circulars portal |

| Insurance Information Bureau of India (IIB) | Insurance information services, data-related resources, and policy-information support linked to the insurance ecosystem | https://iib.gov.in/ |

| Your insurer’s official website | Current policy wording, add-on details, renewal notices, endorsement wording, and product brochures for your exact bike insurance policy | Check the official website of your insurer listed in your policy schedule |

| Your policy schedule / renewal notice | The actual endorsements, deductibles, premium adjustments, and wording applicable to your own two-wheeler policy | Available directly in your issued policy document or renewal communication |

Note: IMT descriptions in articles are useful for understanding the basics, but the final applicable wording is always the version shown in the official policy documents and current regulatory framework.

Glossary Of Imt Terms Used In This Article

Here are the most common IMT Terms used in this article:

| Term | Meaning | Why it matters |

|---|---|---|

| IMT | Indian Motor Tariff. This is the standard framework used in motor insurance for endorsements, conditions, premium rules, and policy wording related to vehicles. | It helps you understand the rules behind your policy and any special endorsements attached to it. |

| Endorsement | A written change or addition made to the policy. It can extend, limit, clarify, or modify the original cover. | This is how IMTs and other policy changes are officially added. |

| Endorsement schedule | The part of the policy that lists all endorsements, add-ons, discounts, special conditions, and other policy modifications applicable to your vehicle. | It shows the exact extra terms attached to your policy. |

| Policy schedule | The main summary page of your insurance policy. It usually contains the insured vehicle details, policy period, IDV, premium breakup, deductibles, and endorsements. | This is the quickest place to verify what is actually covered. |

| Premium | The amount you pay to buy or renew the insurance policy. It may include separate charges for own-damage cover, third-party cover, add-ons, and taxes. | It is the cost of your insurance cover. |

| OD | Own Damage. This is the part of the policy that covers damage to your own bike due to events such as accident, fire, theft, flood, or other insured risks. | Most add-ons and deductibles affect this section. |

| TP | Third Party. This refers to legal liability for injury, death, or property damage caused to another person or their property by your insured vehicle. | It is the legal protection you need if your bike causes harm to others. |

| Third-party liability | The insurer’s responsibility to pay for damage, injury, or death caused to others by your bike, subject to the policy terms and legal limits. | This is one of the most important cover types in motor insurance. |

| IDV | Insured Declared Value. This is the approximate current insured value of the bike, usually based on depreciation from its original value, and it often acts as the maximum payout in total-loss or theft claims. | It strongly affects your premium and claim payout. |

| CSI | Capital Sum Insured. This is the fixed amount insured under personal accident cover, such as owner-driver or unnamed passenger personal accident benefits. | It sets the payout limit for personal accident cover. |

| Sum insured | The maximum amount the insurer agrees to pay under a specific section of the policy or add-on cover, subject to terms and exclusions. | It tells you the upper limit of protection for that cover. |

| Deductible | The portion of a claim that you must pay yourself before the insurer pays the remaining eligible amount. | It directly reduces the claim amount you receive. |

| Excess | Another term often used for deductible. It means the amount that remains your responsibility in every applicable claim. | It helps readers understand claim deductions in simpler language. |

| Compulsory deductible | The fixed minimum amount that every policyholder must bear in an own-damage claim as per applicable tariff or insurer rules. | It applies automatically in eligible claims. |

| Voluntary deductible | An extra deductible chosen by the policyholder in exchange for a lower premium. It reduces premium cost, but increases your out-of-pocket expense during a claim. | It can save money, but only if you are comfortable with a higher claim-time cost. |

| Pro-rata | A partial calculation based on time or proportion. For example, if a discount or refund applies only to part of the policy period, it may be calculated on a pro rata basis. | It explains partial premium adjustments and refunds. |

| Add-on cover | An optional extra cover purchased in addition to the base policy to protect against specific risks or improve claim benefits. | It lets you customise the policy for better protection. |

| Accessories | Extra items fitted to the bike apart from the standard factory setup, such as chargers, fog lamps, GPS units, mobile holders, or other declared fittings. | Accessories may need to be declared separately for cover. |

| Declared accessories | Accessories whose value has been disclosed to the insurer and included in the policy for premium calculation and claim eligibility. | Only declared items are usually eligible for accessory cover. |

| Exclusions | Situations, losses, or damages that the policy does not cover. These are important because even a valid policy does not pay for everything. | This tells you what the insurer will not pay for. |

| Depreciation | The reduction in the value of the vehicle or its parts over time because of age, wear, and usage. This affects claim calculations and IDV. | It can reduce the amount payable in a claim. |

| Claim | A formal request made by the policyholder to the insurer for compensation after a covered loss or damage. | This is how you ask the insurer to pay for a covered event. |

| Own-damage claim | A claim made for loss or damage to your own bike under the own-damage section of the policy. | Most IMT add-ons and deductibles affect own-damage claims. |

| Total loss | A situation where the vehicle is damaged beyond economical repair or the repair cost exceeds the insurer’s permitted threshold compared with the IDV. | It is one of the most important claim outcomes to understand. |

| Renewal notice | A communication from the insurer before policy expiry that reminds you to renew the policy and may include updated premium or cover details. | It helps you renew on time and avoid policy breaks. |

| Proposal form | The form filled by the policyholder while buying or renewing insurance. It includes declarations about the vehicle, accessories, usage, and the selected cover. | It is the basis for issuing the policy correctly. |

| Insured | The person in whose name the insurance policy is issued and who is entitled to policy benefits, subject to the terms and conditions. | This identifies who gets the insurance protection. |

| Insurer | The insurance company that issues the policy and settles valid claims according to the policy wording. | This is the company responsible for paying eligible claims. |

| Personal accident cover | A benefit that pays a fixed amount in case of accidental death or specified disability of the insured person covered under that section. | It is a key protection for riders and pillion-related risk in some policies. |

| Schedule | A general insurance term referring to the document section that summarises details specific to your policy, such as insured values, endorsements, premium, and insured items. | It is the easiest place to check the exact cover you bought. |

What Are The Common Mistakes To Avoid?

Two-wheeler insurance often seems simple at first, but many claim issues arise because riders miss small details in the policy. Here are some common mistakes to avoid:

- Forgetting to declare accessories such as chargers, lights, GPS units, or other fitted items can leave those items uncovered when a claim is made.

- Ignoring voluntary deductibles; they can reduce your premium, but they also increase the amount you must pay yourself during a claim.

- Confusing compulsory deductibles with voluntary deductibles, assuming the insurer will pay the full claim amount. In reality, deductibles always reduce the payout in own-damage claims, so it is important to check both amounts in the policy document.

- Assuming every endorsement applies everywhere, when some covers are meant only for special situations, such as cross-border travel or use on private premises.

- Misunderstanding exclusions. Even if you buy an add-on, normal exclusions such as wear and tear, mechanical breakdown, or unauthorised use may still apply.

- Relying solely on the article or brochure, the actual terms that apply to your bike are those printed in the policy schedule issued by the insurer.

Faqs On Indian Motor Tariff (imt) For Two-wheelers In India

1. What Is The Indian Motor Tariff (imt)?

IMT stands for Indian Motor Tariff, which defines the rules, endorsements, and coverage options for motor insurance policies in India, including two-wheelers.

2. Which Imts Are Essential For Most Two-wheeler Owners?

IMT-22 (compulsory deductible) and IMT-15 (personal accident cover for owner-driver) are considered essential. Others, such as IMT-22A, IMT-24, and IMT-33, are optional based on your needs.

3. How Does The Imt-22 Compulsory Deductible Affect My Claim?

For every own-damage claim, you must pay the first ₹50 out of pocket; the insurer pays the rest. This does not apply to third-party claims.

4. Can I Get A Premium Discount For Fitting An Anti-theft Device?

Yes, under IMT-10, if your two-wheeler is equipped with an ARAI-certified anti-theft device, you are eligible for a 2.5% discount (up to ₹500) on the own-damage premium.

5. What Is The Benefit Of Being A Member Of An Automobile Association?

IMT-8 provides a 5% discount (up to ₹50) on the own-damage premium if you are an active member of a recognised automobile association.

6. What Is A Voluntary Deductible (imt-22a)?

It is an extra deductible you agree to pay per claim in exchange for a lower premium. You can choose the amount, but it increases your out-of-pocket cost during a claim.

7. How Can I Cover Electrical Or Electronic Accessories?

IMT-24 allows you to insure declared electrical/electronic accessories by paying an extra premium (4% of their value). Only declared items are covered.

8. What Is Covered Under Loss Of Accessories (imt-33)?

IMT-33 insures declared accessories against theft, burglary, or housebreaking—but not accidental damage. You pay an additional premium (typically 3% of the value of the accessories).

9. Can I Extend My Insurance To Cover Riding In Other Countries?

Yes, IMT-1 extends coverage to select neighbouring countries, such as Nepal, Bhutan, and Sri Lanka, for an additional premium.

10. Where Can I Check For The Latest Imt Updates And Policy Changes?

You should check the IRDAI website, your insurer’s official website, and your policy schedule for the most current IMT rules and endorsements.

Other Related Articles From Bikeleague India

- Bike insurance jargons & addons in India Guide

- Two wheeler insurance in India – How to buy and select

- Bike insurance tips in India – Tips to get a lower premium

- What all basic motorcycle accessories should a rider have

- Bike IDV Calculator – Calculate Your Bike’s Value Online

Conclusion

Indian Motor Insurance Tariff (IMT) endorsements can seem complicated at first, but learning how they affect your two-wheeler insurance can help you save money, get better coverage, and avoid costly mistakes.

Choosing the right mix of compulsory and voluntary deductibles, add-on covers, and declared accessories helps make sure your policy fits your real needs. Discounts for anti-theft devices or association memberships can also help keep your premiums affordable.

Always check your policy schedule, look at the latest official guidelines, and ask questions if you’re not sure about your coverage. With the right information, you can ride with confidence, knowing your insurance suits you.

We hope this article has answered your main questions about Indian Motor Tariffs for two-wheelers. If you have more questions, you can email us at bikeleague2017@gmail.com or leave a comment below. We’re always happy to help. You can also connect with Bikeleague India on social media.