Long story short: Discover the key factors affecting bike loan interest rates in India. Get the insights you need to make informed decisions.

Getting a new bike is exciting, but it’s important to understand how bike loan interest rates work before you apply. In India, these rates depend on several factors. Some you can control, while others are set by lenders or the market. Knowing what affects your

An interest rate helps you make better financial choices, avoid extra costs, and get a good deal. This guide will walk you through the main factors so you can buy your next bike with confidence.

Key Takeaways

- Your credit score is the single most important factor influencing bike loan interest rates in India. A high score can help you secure lower rates, while a low score may result in higher rates or even loan rejection.

- Stable income and employment history boost your chances of getting a favourable interest rate, as lenders see consistent earnings as a sign of reliable repayment capacity.

- Making a larger down payment and opting for a shorter loan tenure generally leads to more competitive interest rates and lower overall interest costs.

- Market conditions, government policies, and competition among lenders can all impact the rates on offer, so it pays to compare options and stay informed about economic trends.

- Additional charges—such as processing fees, documentation charges, and penalties—can significantly increase your total loan cost, so always review the fine print before signing any agreement.

What Are The Key Factors Affecting Bike Loan Interest Rate In India?

| Factor | Effect on Interest Rate | Why it Matters |

|---|---|---|

| High credit score (750+) | Lowers rate | Signals strong repayment behaviour and lower lender risk. |

| Stable income | Lowers rate | Shows consistent repayment capacity. |

| Larger down payment | Lowers rate | Reduces the loan amount and lender exposure. |

| Shorter loan tenure | Often lowers rate | Reduces risk for the lender, though EMI becomes higher. |

| Good relationship with lender | May lower rate | Existing customers may get better pricing or special offers. |

| Government policy support | May lower rate | Subsidies or incentives can reduce borrowing costs in some cases. |

| Low credit score (below 650) | Raises rate or causes rejection | Indicates higher credit risk. |

| Unstable employment | Raises rate | Irregular income makes repayment less predictable. |

| High loan amount | Raises rate | Increases lender risk, especially relative to income. |

| Long loan tenure | Raises total interest cost | Lowers EMI but increases overall interest paid. |

| Low down payment | Raises rate | Increases loan-to-value ratio and lender risk. |

| Unfavourable market conditions | Raises rate | Inflation and tighter monetary policy usually push rates up. |

| Premium or imported bike | May raise rate | Higher cost and resale risk can affect pricing. |

| Negative credit history | Raises rate or causes rejection | Defaults and late payments reduce lender confidence. |

| Strong lender competition | May lower rate | Lenders may offer better deals to attract customers. |

| Regulatory changes | May raise or lower rate | New rules can change pricing and eligibility norms. |

1. High Credit Score

Keeping your credit score above 750 can help lower your interest rate. Lenders see people with high credit scores as less risky to lend to.

2. Stable Income

A steady and reliable income, like a regular job or business earnings, can help you get a lower interest rate.

3. Large Down Payment

Making a bigger down payment means you borrow less, which can lead to better loan terms and a lower interest rate.

4. Loan Tenure

If you choose a shorter loan period, you might get a lower interest rate. However, your monthly payments will be higher.

5. Relationship With The Lender

If you have a good history with your bank or lender, you might qualify for better interest rates.

6. Government Policies

Sometimes, the Indian government or RBI introduces policies to make it easier to get loans for certain vehicles, like motorcycles, by offering subsidies or lower interest rates.

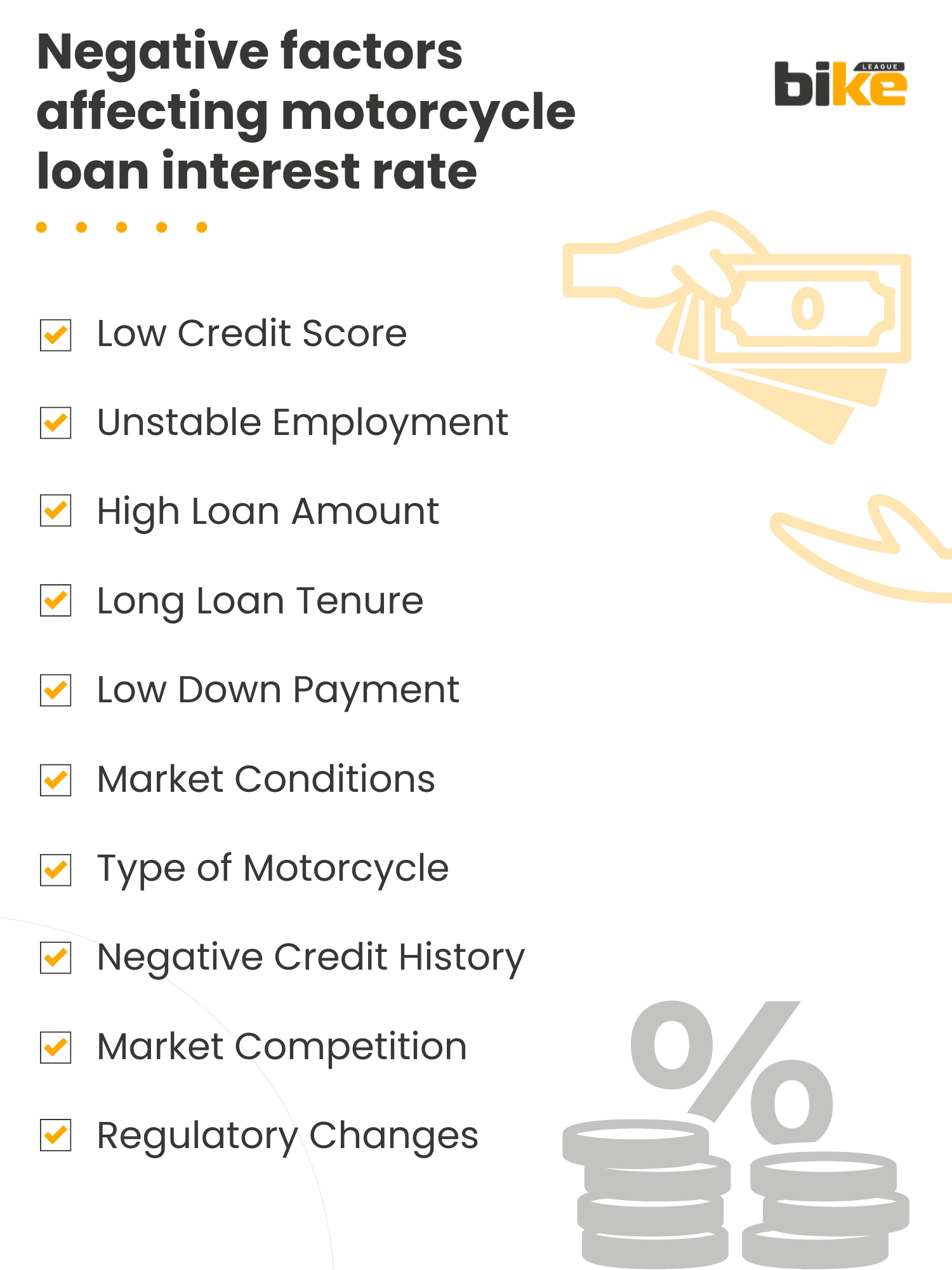

What Are The Negative Factors Affecting Bike Loan Interest Rates In India?

1. Low Credit Score

A credit score below 650 is seen as low and can hurt your chances of getting a loan. It may lead to higher interest rates or even rejection, as it signals higher risk to lenders.

2. Unstable Employment

If you change jobs often or have an irregular income, lenders may see you as a higher risk. This can mean higher interest rates.

3. High Loan Amount

Taking a large loan compared to your income can lead to higher interest rates, as it increases the lender’s risk.

4. Long Loan Tenure

A longer loan term can lower your monthly payments, but you’ll end up paying more interest overall.

5. Low Down Payment

If you make a small down payment, your loan amount is higher compared to the bike’s value. This can lead to higher interest rates because it’s riskier for the lender.

6. Market Conditions

When the economy isn’t doing well, like during high inflation or strict monetary policies, interest rates usually go up.

7. Type Of Bike

Some bikes, especially expensive or imported ones, can have higher interest rates because they cost more and are seen as riskier.

8. Negative Credit History

If you’ve missed payments or defaulted on loans before, you might face higher interest rates or even have your loan application denied.

9. Market Competition

Competition between lenders can sometimes lower interest rates, but not always. If lenders become stricter with their checks, you might not benefit.

10. Regulatory Changes

Changes in lending rules or government policies can impact interest rates and loan terms.

What Steps Can I Take To Improve My Credit Score Before Applying For A Bike Loan In India?

To improve your credit score before applying for a bike loan in India, follow these steps:

1. Check Your Credit Report For Errors

Get your credit report from bureaus like CIBIL, Equifax, or Experian. Dispute any inaccuracies that could harm your score.

2. Pay Bills And Emis On Time

Always pay at least the minimum due on credit cards and EMIs before the due date. Late payments can hurt your score, so consider setting up an auto-debit.

3. Maintain A Low Credit Utilisation Ratio

Keep credit card usage below 30% of your limit. For example, if your limit is ₹1,00,000, use only ₹30,000 or less.

4. Settle Outstanding Dues And Reduce Debt

Pay down high-interest debts. Negotiate with lenders if needed and ensure closed accounts are marked as ‘Closed’ in your report.

5. Avoid Multiple Loan Applications

Limit new loan applications to reduce hard inquiries that can negatively affect your score. Apply only when eligible.

6. Maintain A Good Credit Mix

Have a mix of secured (home/car loans) and unsecured credit (credit cards). If you only have credit cards, consider taking a small secured loan.

7. Don’t Close Old Credit Accounts

Keep your oldest accounts active to enhance your credit history and score.

8. Regularly Monitor Your Credit Score

Check your score frequently, as updates now happen every 15 days. This helps you catch errors quickly.

9. Clear Outstanding Dues Instead Of Defaulting

Try to settle overdue loans rather than defaulting. This can gradually restore your credit score.

10. Use Emi Options Responsibly

Ensure timely repayments on EMI purchases, as they impact your credit history.

What Hidden Fees And Charges Should You Be Aware Of When Dealing With Motorcycle Lenders In India?

When you get a motorcycle loan in India, watch out for hidden fees that can raise your total cost. Even if lenders say there are “no hidden fees,” extra charges are common. Here are some fees to look out for:

| Charge | Typical Impact | What to Note |

|---|---|---|

| Processing fee | Upfront cost | Usually charged before or at loan disbursal. |

| Documentation charges | Administrative cost | May be bundled with processing charges. |

| Stamp duty and RTO charges | State-dependent cost | Usually non-refundable. |

| RC collection fee | Small one-time fee | Related to registration paperwork. |

| Foreclosure or prepayment fee | Cost for early closure | Can reduce savings from early repayment. |

| EMI bounce penalty | Charge per missed payment | Often includes penal interest too. |

| Loan cancellation charges | Can be significant | May include processing fee and statutory costs. |

| Repayment mode change fee | Minor extra charge | Applies if you switch payment method. |

| Legal, repossession, or PDD fees | Varies by case | Usually applies when documentation or repayment is delayed. |

| Cash EMI collection charge | Extra service fee | Applies if payment is collected in cash. |

| RC hypothecation delay fee | Penalty for delayed formalities | Avoidable by completing documents on time. |

- Processing Fee: Usually 1-5% of the loan amount, charged upfront. For example, HDFC Bank charges up to 2.5%, Bajaj Finance up to 5%, and SBI 2%.

- Documentation Charges: Range from ₹750 to 2.25% of the loan amount, sometimes combined with processing fees.

- Stamp Duty/RTO Charges: Based on state law; deducted upfront and generally non-refundable if the loan is cancelled.

- Registration Certificate (RC) Collection Fees: A one-time fee of around ₹885 for paperwork.

- Foreclosure/Prepayment Charges: Most banks charge 1-5% of the outstanding principal if you repay early, with Bajaj Finserv charging up to 4.72%.

- Penalty for Loan Default/EMI Bounce: Typically ₹339–₹1,500 per bounced payment plus penal interest, which can be 8% annualised.

- Loan Cancellation: If you cancel after disbursal but within a short period, you may owe the full processing fee, interest accrued, and statutory duties.

- Change of Repayment Mode/Instrument Swap: Charges may apply, starting around ₹500.

- PDD Collection, Legal, and Repossession Fees: These can range from a few hundred to several thousand rupees for delayed processes.

- DCC Charge (Cash EMI Collection): Expect an extra fee per cash transaction, reaching up to ₹1,500.

- Delay in RC Hypothecation: A fee of up to ₹1,500 may apply if registration formalities are delayed.

What Are The Steps To Improve A Credit Score In India?

Raising your credit score before you apply for a bike loan in India can help you get better interest rates and boost your chances of approval. Lenders look at your payment history, how much credit you use, your current debts, and your overall financial habits when deciding your loan terms.

The table below shows the best steps you can take to improve your credit profile and make yourself a stronger candidate for banks and lenders.

| Step | What to Do | Result |

|---|---|---|

| Check credit report | Review reports from bureaus and correct errors. | Removes mistakes that may lower your score. |

| Pay on time | Pay EMIs and card dues before due date. | Builds positive repayment history. |

| Keep credit use low | Try to stay below 30% utilisation. | Supports a healthier credit score. |

| Clear overdue dues | Reduce outstanding balances and settle missed payments. | Improves repayment profile over time. |

| Avoid too many applications | Apply for credit only when necessary. | Limits hard inquiries on your report. |

| Maintain credit mix | Keep a mix of secured and unsecured credit. | Can strengthen your credit profile. |

| Keep old accounts open | Do not close long-standing credit lines unnecessarily. | Preserves credit history length. |

| Monitor regularly | Check your score frequently. | Helps catch issues early. |

| Avoid defaulting | Settle overdue payments instead of ignoring them. | Prevents long-term score damage. |

| Use EMIs responsibly | Repay instalments on time. | Adds to a positive credit record. |

Faq Related To Key Factors Affecting Bike Loan Interest Rate

1. Is A Motorcycle Loan Interest Tax Deductible?

In India, motorcycle loan interest is usually not tax-deductible. Unlike home loans or education loans, which may provide tax benefits under specific sections of the Income Tax Act, motorcycle loans are personal loans. Therefore, the interest paid on them is not eligible for income tax deductions or exemptions.

2. Which Bank Offers The Lowest Interest Rate For A Bike Loan?

Several factors, including your credit score, loan amount, tenure, and current market conditions, can influence which bank offers the lowest interest rate for a bike loan. Additionally, interest rates on bike loans can fluctuate over time.

3. What Is The Standard Bike Loan Interest Rate In India?

Bike loan interest rates in India vary depending on several factors, including the lender, the applicant’s creditworthiness, the loan tenure, and the prevailing market conditions. Interest rates for bike loans in India range from 9% to 24% annually.

4. What Is The Most Important Factor That Affects My Bike Loan Interest Rate?

The borrower’s credit score is the most critical factor influencing bike loan interest rates. A high credit score can lead to more favourable loan terms, reflecting the borrower’s creditworthiness and ability to repay the loan.

5. How Does My Income Affect My Bike Loan Interest Rate?

Your monthly income and employment stability are significant factors in determining your bike loan interest rate. Lenders assess your repayment capacity based on your income and job stability, which can influence the interest rate you receive.

6. Does The Type Of Bike I Want To Buy Affect The Interest Rate?

Yes, the type of bike you intend to purchase can impact the interest rate. Different models may have varying risk profiles, which lenders consider when setting interest rates.

7. Will Making A Bigger Down Payment Lower My Interest Rate?

Making a larger down payment could lower your interest rate. A substantial down payment reduces the loan amount and the lender’s risk, which may result in a more favourable interest rate.

8. How Do Market Conditions Affect Bike Loan Interest Rates?

Market conditions, including RBI policy rates and inflation, are crucial in determining bike loan interest rates. Changes in these economic factors can lead to fluctuations in interest rates offered by lenders.

9. What Role Does The Lending Institution Play In Determining Interest Rates?

The lending institution’s policies and relationship with the borrower can influence the interest rate. Different lenders may offer varying rates based on their internal credit policies and the borrower’s history with them.

10. How Does Loan Tenure Affect The Interest Rate?

The loan tenure is a key factor in determining the interest rate. Generally, shorter loan tenures attract lower interest rates as they pose less risk to the lender.

11. Are There Any Additional Charges Associated With Bike Loans?

Yes, bike loans often come with additional charges such as processing fees, documentation charges, and penalties for late payments or prepayment. These fees can affect the overall cost of the loan.

12. What Is The Impact Of Competition Among Lenders On Interest Rates?

Competition among lenders can lead to more competitive interest rates. When multiple lenders vie for customers, they may offer lower rates to attract borrowers.

Other Related Articles From Bikeleague India

- Bike Loan calculator | Quick and Easy Calculation

- Motorcycle loan – How to finance your dream bike

- Statewise & Union Territory Two Wheeler Road Tax in India

- Calculators converters for bikes In India

- Two Wheeler Road Tax in India: A Detailed Explanation

Conclusion

Knowing what affects bike loan interest rates in India helps you make better financial decisions when buying a two-wheeler. Pay attention to your credit score, keep your income steady, make a reasonable down payment, and stay updated on market trends and lender rules. Compare different lenders, read all the details, and plan your loan carefully. With this knowledge, you can get a good deal and enjoy your new bike with confidence.

We’ve covered all the main factors that affect bike loan interest rates, both good and bad. If you have questions, feel free to email us at bikeleague2017@gmail.com or leave a comment below. We’re here to help you.