Long story short – As the law mandates, every motorcycle or two-wheeler owner in India should have mandatory third-party bike insurance per the Motor Vehicles Act 1988. Also, comprehensive or bumper-to-bumper insurance is the best for motorcycle/ bike insurance, without a doubt.

Owning a motorcycle or scooter in India brings freedom and convenience, but it also comes with important responsibilities—chief among them is securing proper insurance coverage. With the ever-increasing number of two-wheelers on Indian roads and the associated risks, understanding your insurance options is not just a legal necessity but also essential for your financial safety and peace of mind. This comprehensive guide will help you navigate the laws, coverage types, key factors, and practical tips to make informed decisions about two-wheeler

insurancein India

Key Takeaways

- Third-party insurance is legally mandatory for all two-wheeler owners in India, as per the Motor Vehicles Act. Riding without it can result in severe legal and financial consequences.

- Comprehensive and bumper-to-bumper (zero depreciation) insurance policies offer the broadest protection, covering both third-party liabilities and damages to your own vehicle—including depreciation-free claims with bumper-to-bumper plans.

- Insurance premiums are influenced by factors such as location (urban vs rural), rider experience, and the type of coverage chosen. Urban areas and inexperienced riders typically face higher premiums.

- Add-ons like zero depreciation, engine protection, roadside assistance, and No Claim Bonus (NCB) protection can enhance coverage but come at an extra cost. Choosing the right add-ons depends on your riding habits, location, and bike value.

- Always review policy exclusions, maintain valid documentation, and renew your policy on time to avoid claim rejections and ensure continuous protection.

How to buy or select two-wheeler insurance?

Motorcycle insurance is the first thing that comes to mind for a new two-wheeler owner. Most people need to learn the basics of insurance and get lured by an insurance agent’s words. If an accident occurs, they do not even know which type of bike insurance policy they hold, and they have yet to learn all the steps to take. So, let’s get to the basics of motorcycle insurance, like how to buy, select, and exclude two-wheeler insurance, and we will simplify this tedious task. First, let’s discuss the types of motorcycle insurance.

What is the legal mandate for Motorcycle Insurance in India?

1. Compulsory Insurance Under the Motor Vehicle Act

Under the Motor Vehicles Act 2019, India requires bike owners to have a third-party liability insurance policy. This requirement ensures that bike owners are legally covered for any damages caused to third parties in the event of an accident. Failure to comply with this law can result in fines or imprisonment.

2. Five-Year Insurance Requirement for New Bikes

The Insurance Regulatory and Development Authority of India (IRDAI) mandates that new bike purchases include a 5-year third-party insurance policy and a 1-year own-damage insurance policy. This long-term bike insurance policy reduces the hassle of annual renewals and ensures continuous coverage.

What are the consequences of not having motorcycle insurance?

1. Legal Penalties

Riding a motorcycle without insurance is a legal offence in India. Non-compliance with the mandatory insurance requirement can lead to significant fines and legal consequences, including imprisonment. This strict enforcement underscores the importance of adhering to the insurance mandate.

2. Financial Risks

Without insurance, motorcycle owners face substantial financial risks. In the event of an accident, they would have to bear the total cost of damages and medical expenses, which can be financially crippling. Insurance mitigates these risks by providing necessary financial support and coverage.

Types of two-wheeler insurance in India

1. Third-Party bike Insurance

In simple terms, third-party insurance must be mandatory for all vehicles in India. The rates are set annually by IRDAI (Insurance Regulatory & Development Authority of India) and cover only third-party liabilities and expenses. It provides financial protection against damages or injuries caused to a third party by the insured vehicle.

Pros of third party bike Insurance

- Legal Compliance: Third-party bike insurance is mandatory by law for all two-wheeler owners in India, ensuring legal compliance.

- Cost-Effective: It is generally less expensive as the premium rates are predefined by the Insurance Regulatory and Development Authority of India (IRDAI).

- Quick and Simple Purchase: The process of buying bike third-party insurance is straightforward and can often be completed online.

Cons of third party bike Insurance

- Limited Coverage: This type of insurance only covers damages to third-party persons and property, leaving the owner without coverage for their own vehicle.

- No Own Damage Coverage: It does not provide financial protection for damages to the insured vehicle, which can be a significant drawback.

- Complex Claim Process: The claim process can be complex and time-consuming, involving legal proceedings and documentation.

2. Standalone Own Damage (OD) two-wheeler Insurance

Standalone Own Damage insurance covers damages to the insured two-wheeler due to accidents, theft, fire, or natural disasters. This type of bike insurance policy benefits those who already have third-party bike insurance but want additional coverage for their own vehicle.

Pros of Standalone Own Damage insurance

- Coverage for Own Vehicle: OD insurance covers damages to your own vehicle due to accidents, theft, fire, natural disasters, and other perils.

- Customisation Options: You can enhance your OD insurance with add-ons such as zero depreciation cover, roadside assistance, and engine protection.

- Peace of Mind: It provides financial protection against a wide range of risks, giving you peace of mind.

Cons of Standalone Own Damage insurance

- Higher Premium: OD insurance generally has a higher premium compared to third-party insurance.

- Depreciation Consideration: Insurers may consider depreciation while settling claims, resulting in a lower compensation amount.

3. Comprehensive two-wheeler insurance

In the comprehensive plan, in addition to third-party coverage, expenses for loss/damage to your vehicle, personal accident cover for the driver and rider, third-party bodily injury, and damage to the owner’s vehicle are covered. We can also add additional riders (add-ons) to the existing policy. Plastic coverage is considered, but depreciation rates apply.

Pros of Comprehensive two wheeler insurance

- Broad Coverage: Comprehensive insurance covers both own vehicle damages and third-party liabilities, providing extensive protection.

- Additional Coverage Options: It offers various add-ons such as personal accident cover, consumables cover, and roadside assistance.

- Peace of Mind: With comprehensive coverage, you are protected against a wide range of risks, including accidents, theft, fire, and natural disasters.

Cons of Comprehensive two wheeler insurance

- Higher Premium: Comprehensive insurance generally has a higher premium compared to OD and third-party insurance due to the broader coverage it provides.

- Exclusions and Limitations: There may be certain exclusions and limitations in the bike insurance policy, such as deductibles, waiting periods, and specific conditions for coverage.

4. Bumper to Bumper two-wheeler insurance

Bumper-to-bumper insurance, also known as zero depreciation or nil depreciation cover, is an add-on to a comprehensive bike insurance policy and is the best and most expensive motorcycle insurance plan. All the features in the comprehensive plan are included in this plan. Everything is covered under this plan, including plastic parts in the event of an accident. Depreciation rates are not applicable under this plan, even for plastic parts and are valid for the first 5 years of ownership.

Pros of Bumper to Bumper insurance

- No Depreciation Consideration: Bumper-to-bumper insurance ensures that you can claim the full insured amount for your vehicle without any depreciation deductions.

- Enhanced Coverage: It provides slightly broader coverage compared to comprehensive insurance, including coverage for all metal parts, fibre, and rubber.

- Higher Claim Amount: The claim amount is higher because the insurer does not deduct depreciation from the parts of the vehicle that have been repaired or replaced.

Cons of Bumper to Bumper insurance

- Higher Premium: The premium for bumper-to-bumper insurance is higher due to the additional zero depreciation cover.

- Limited Claims: Insurers may limit the number of claims allowed under bumper-to-bumper insurance.

- Exclusions: It may not cover damages to tyres, engine, or gearbox due to water ingression or oil leakage.

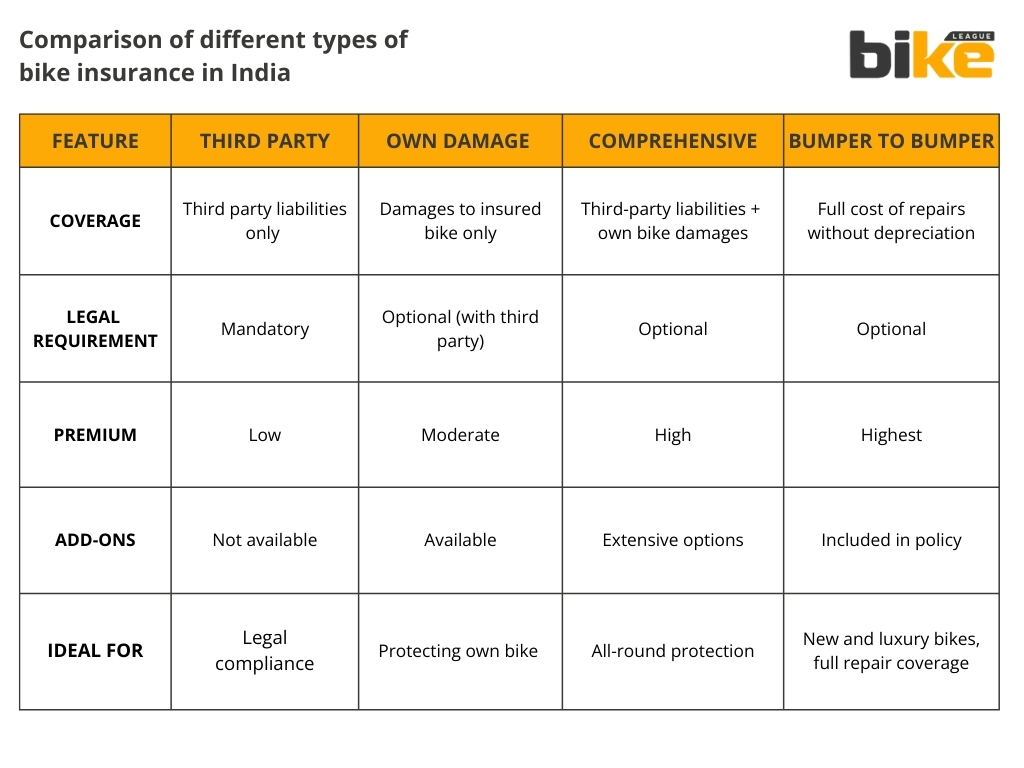

| Feature | Third Party only | Own Damage | Comprehensive | Bumper to Bumper |

|---|---|---|---|---|

| Coverage | Third party liabilities only | Own damages only | Third party liabilities + Own bike damages | Full cost repairs without depreciation |

| Legal Requirement | Mandatory | Optional (with third party) | Optional | Optional |

| Premium | Low | Moderate | High | Highest |

| Add-ons | Not available | Available | Extensive options | Included in policy |

| Best for | Legal compliance | Protecting own bike | All-round protection | New and luxury, full repair coverage |

What’s not covered in two-wheeler insurance in India?

1. Driving Under the Influence

Insurance policies do not cover damages if the rider is found driving under the influence of alcohol or drugs. This is a standard exclusion across all policies to discourage irresponsible behaviour and ensure road safety.

2. Lack of Valid Documentation

Claims are rejected if the rider does not possess valid documents, such as a driver’s license or insurance certificate, at the time of the accident. This exclusion emphasises the importance of adhering to legal requirements while riding.

3. Mechanical or Electrical Failures

Damages resulting from mechanical or electrical faults in the vehicle are not covered. These issues are part of regular maintenance and the owner’s responsibility.

4. Regular Wear and Tear

Insurance policies do not cover damage caused by the regular wear and tear of vehicle components. This exclusion ensures the policy is used for unforeseen events rather than routine maintenance.

5. Geographical Limitations

Accidents that occur outside the policy’s specified geographical boundaries are not covered. This exclusion is crucial for riders who frequently travel across different regions.

6. Purposeful Damage

Any damage caused intentionally to raise a fraudulent claim is not covered. This exclusion helps prevent insurance fraud and ensures that only genuine claims are honoured.

7. Expired Policy

Claims made on a lapsed or inactive bike insurance policy are not entertained. It is essential to renew the policy on time to maintain continuous coverage and avoid claim rejections.

8. Riding Without a Helmet

Some policies exclude coverage if the rider is not wearing a helmet at the time of the accident. This exclusion promotes the use of safety gear and reduces the risk of severe injuries.

9. Overspeeding

Accidents caused by overspeeding are often not covered. This exclusion encourages safe riding practices and reduces the likelihood of high-speed accidents.

10. Theft Due to Negligence

The claim may be rejected if the vehicle is stolen due to the owner’s negligence, such as leaving the keys in the ignition. This exclusion underscores the importance of taking basic precautions to prevent theft.

11. Third party Damages

An own-damage bike insurance policy does not cover damage to third parties. Separate third-party bike insurance is required to cover such liabilities.

12. Accidents as a Passenger

Accidents that occur while the insured person is a passenger on someone else’s two-wheeler are not covered. This exclusion clarifies that coverage is limited to the insured vehicle.

13. Protective Gear Damage

Damage to the helmets or other protective gear is generally not covered under standard two-wheeler insurance policies. Riders may need to purchase additional coverage for such items.

How do motorcycle insurance premiums vary based on location in India?

Motorcycle insurance premiums in India vary significantly based on location. Let’s explore how these factors impact insurance rates.

Urban vs. Rural Areas

Urban Areas

Generally have higher insurance premiums due to several factors:

- Increased traffic congestion

- Higher accident rates

- Elevated theft risks

- Greater population density

- Higher crime rates

Rural Areas

Typically benefit from lower insurance premiums due to:

- Reduced traffic

- Lower accident rates

- Decreased overall risk for insurers

State-Specific Variations

Insurance premiums can vary between states due to:

- Differing local regulations

- Unique risk assessments

- Traffic volumes

- Theft rates

For instance, coastal states like Tamil Nadu, which are prone to cyclones, may have higher premiums than inland states like Bihar due to the elevated risk of weather-related damage.

How do motorcycle insurance premiums vary based on rider experience in India?

Rider experience is another significant factor influencing motorcycle insurance premiums in India:

1. Experienced Riders

Generally considered lower risk by insurers.

Often benefit from lower insurance premiums.

Perceived to have better riding skills and be less likely to be involved in accidents

2. Inexperienced Riders

Typically, they face higher premiums due to increased risk perception

3. Riding Record

A clean riding record, free from accidents and traffic violations, can significantly reduce insurance premiums

Riders with a history of claims or violations are often seen as high-risk, leading to higher premiums

4. Duration of Riding

The length of time a rider has been riding influences premiums

Insurers may require 2 to 5 years of good riding habits before offering reduced rates

5. Safety Practices

Adhering to safe riding practices and following traffic rules can enhance a rider’s profile

Safe riders are eligible for lower premiums as they reduce the likelihood of accidents and claims

What is Insured Declared Value (IDV)?

IDV, or Insured Declared Value, represents the maximum amount an insurance company will compensate in case of total loss or theft of your bike. It is the current market value of your motorcycle, adjusted for depreciation. The IDV is crucial because it determines the maximum payout you can receive from your insurer in the event of a total loss or theft.

1. Calculation of IDV

The IDV is calculated based on the bike’s manufacturer’s selling price minus the depreciation rate applicable to its age and parts. Factors such as the bike’s make and model, registration date, city of registration, fuel type, and age are considered when determining the IDV.

2. IDV Impact on Premium and Coverage

IDV directly affects the insurance premium: a higher IDV results in a higher premium but provides better financial protection. Conversely, a lower IDV might reduce the premium and decrease coverage. It is essential to balance adequate coverage and manageable premiums by choosing an IDV that aligns with your bike’s value and budget.

3. IDV Depreciation and Adjustments

Depreciation plays a significant role in calculating the IDV. Older bikes depreciate faster, resulting in lower IDVs. The IDV is typically fixed at the policy’s inception but may be adjusted during renewal, subject to mutual agreement between the insurer and policyholder.

What is No-Claim Bonus?

NCB, or No Claim Bonus, is a discount the insurer awards for not raising any claims during the policy period. It serves as a reward for safe riding and helps reduce the premium for the subsequent policy period. The NCB can significantly lower the premium’s Own Damage (OD) component.

1. Calculation and Accumulation of NCB

The percentage of NCB increases with each consecutive claim-free year, reaching up to 50% for five successive claim-free years. This bonus is applied to the renewal premium, making it a cost-saving benefit for policyholders.

2. NCB Transfer and Protection

When you sell your bike or switch insurers, you can transfer NCB from one bike insurance policy to another. An NCB Protection Add-on Cover can be purchased to safeguard your NCB even if a claim is raised during the policy period. However, the NCB is nullified if the policy is not renewed within 90 days of its expiry.

3. NCB Limitations

NCB is unavailable with third-party Bike Insurance Plans; it only applies to Comprehensive Bike Insurance Policies. The NCB earned on one bike cannot be shared between bike insurance policies or transferred to another person.

What all add-ons are available for two-wheeler insurance?

1. Zero Depreciation Cover

Zero Depreciation Cover ensures that the insurance company covers the full cost of repairs or replacements, without factoring in depreciation. This add-on is highly beneficial as it maximises the claim amount you receive.

2. Engine Protect Cover

The Engine Protect Cover is crucial because it covers engine damage, which is typically not included in a standard comprehensive policy. This add-on is particularly useful in scenarios involving water ingress or oil leakage.

3. Roadside Assistance Cover

Roadside Assistance Cover provides help if you are stranded due to a breakdown or accident. Services may include towing, minor repairs, fuel delivery, and more. This add-on ensures you are not left helpless on the road.

4. Outstation Emergency Cover

This add-on provides assistance if your two-wheeler breaks down or is involved in an accident within a 100 km radius of your residence. It is beneficial for those who frequently travel long distances.

5. Key Protect Cover

Key Protect Cover covers the cost of replacing your bike’s key if it is lost, damaged, or stolen. This add-on can save you the inconvenience and expense of key replacement.

6. Consumables Cover

Consumables Cover includes the cost of consumable items such as engine oil, nuts, bolts, and other materials used during the repair or service of your two-wheeler. This add-on ensures you are not out of pocket for these small but essential items.

7. Personal accident Cover for Pillion Rider

This add-on extends personal accident coverage to the pillion rider, covering medical expenses incurred in an accident. It is a valuable addition for those who often ride with a passenger.

8. Medical Cover

Medical coverage allows the policyholder to claim medical expenses incurred for treatment or hospitalisation following an accident. This add-on provides financial support for medical emergencies.

9. No Claim Bonus (NCB) Protection Cover

NCB Protection Cover ensures that your No Claim Bonus remains intact even if you make a claim during the policy period. This add-on helps maintain your premium discount for the next policy term.

10. Return to Invoice Cover

Return to Invoice Cover ensures that, in the event of total loss or theft, you receive the invoice value of your bike rather than its depreciated value. This add-on is beneficial for new bike owners.

Factors to consider when choosing & selecting Two Wheeler Insurance in India

1. Coverage Options

Ensure the policy provides adequate coverage for damages to your two-wheeler, third-party liability, and personal accident cover.

2. Claim Settlement Ratio (CSR)

A higher CSR indicates a greater likelihood that your claims will be settled promptly.

3. Cashless Garage Network

A vast network of cashless garages lets you get your vehicle repaired conveniently without upfront payments.

4. Additional Covers

Look for policies that offer add-ons such as zero-depreciation cover, roadside assistance, and engine protection cover.

5. Customer Service

Opt for an insurer with good customer service and responsiveness to customer needs.

6. Premium and Discounts

Compare premiums across insurers for similar coverage and look for discounts, such as No Claim Bonus (NCB).

7. Reputation and Financial Stability

Choose an insurance company with a good reputation and financial stability to ensure timely claim settlements.

8. Ease of Purchase and Renewal

Consider the ease of purchasing and renewing the policy, especially if you prefer online transactions.

How to claim for your two-wheeler after an accident?

1. Inform Your Insurer Immediately

Contact Your Insurer: Notify your insurance company about the accident within 24 to 48 hours. Provide detailed information about the accident, including the number of people involved, casualties, and the extent of vehicle/property damage.

Digital Notification: Many insurers offer the convenience of filing a claim through their online platforms or mobile apps, making the process faster and more efficient.

2. File an FIR with the Police (If Required)

Legal Liabilities: If the accident involves legal liabilities or third-party damage, file a First Information Report (FIR) with the police. This step is crucial for claims involving significant damage or third-party involvement.

3. Collect Evidence of the Damages

Photographic Evidence: Take clear pictures of the damage to your bike. This evidence will be essential for the claims process and the surveyor’s assessment.

4. Initiate the Claims Procedure

Online Claim Submission: Visit your insurer’s website or use their mobile app to initiate the claim. Fill out the claims form and upload the required documents, such as copies of your bike insurance policy, FIR, driver’s license, and bike registration certificate (RC).

5. Request a Surveyor

Damage Assessment: After submitting your claim, the insurer will assign a surveyor to assess the damage to your bike. This inspection typically occurs within 2-3 days of submitting your claim.

6. Get Your Bike Repaired

Cashless or Reimbursement: Depending on your policy, you can either opt for a cashless claim at a network garage or get your bike repaired at a garage of your choice and seek reimbursement. In a cashless claim, the insurer directly settles the repair bill with the garage. You must pay the repair costs upfront and then submit the bills to the insurer for reimbursement.

7. Submit Required Documents

Documentation: Ensure you have all the necessary documents ready for a smooth claims process. These typically include:

- Filled and signed claims form

- Driving license

- Bike insurance policy certificate

- Pollution Under Control (PUC) Certificate

- Identity proofs

- Bike Registration Certificate (RC)

- FIR (if required)

- Fire Brigade Report (for comprehensive policies)

- Cancelled cheque

- Original receipts/bills for repairs

How to Download Two Wheeler Insurance Document Online in India

Steps to Download Two Wheeler insurance document from DigiLocker

- Log into DigiLocker: Access your DigiLocker account using your mobile number, Aadhaar number, or username.

- Select the Issuer: Navigate to the ‘Banking and Insurance’ section and select your insurance provider, such as United India Insurance Co. Ltd.

- Choose Policy Type: Select the type of policy you want to download (e.g., two-wheeler insurance).

- Enter Search Parameters: Provide the necessary details like policy number and other required information.

- Fetch Document: Click on ‘Get Document’ after consenting to the terms. Your policy document will be added to the ‘Issued Documents’ section in your DigiLocker account.

Steps to Download from Two Wheeler insurance provider’s App/website

- Visit the Official Website/App: Log in to your insurance provider’s official website or app.

- Navigate to Policy Section: Go to the section where your policies are listed.

- Download Policy Document: Select your bike insurance policy and download the document. Most insurance companies provide a soft copy of the policy.

Which is the best method to take two-wheeler insurance offline or online in India?

Advantages of taking bike insurance online

- Convenience and Time-Saving: Buying and renewing bike insurance online is highly convenient and can be done from the comfort of your home or office at any time of the day, eliminating the need to visit a physical office or wait in long queues.

- Lower Premiums: Online policies often come with lower premiums as they are bought directly from the insurance company, bypassing agent commissions.

- Easy Comparison: The online method allows you to compare policies from different insurance companies easily, helping you make an informed decision and select the best plan that suits your needs.

- Quick and Hassle-Free Process: The process of buying or renewing bike insurance online is straightforward, quick, and paperless, often taking less than five minutes.

- 24×7 Assistance and Add-on Covers: Online platforms offer 24×7 assistance and the option to purchase add-on covers for enhanced protection.

- Retention of No Claim Bonus (NCB): Renewing your bike insurance online allows you to retain your No Claim Bonus (NCB), which provides a discount on your premium for every claim-free year.

- Secure Transactions: Online transactions are secure, with most insurance providers using secure server protocols to ensure a safe environment for purchasing policies.

Disadvantages of taking motorcycle insurance online

- Digital Literacy: Some individuals may find it challenging to navigate online platforms due to a lack of digital literacy or access to the internet.

- Perceived Lack of Personal Touch: The absence of face-to-face interaction with an agent might be a drawback for those who prefer personalised service and guidance.

Advantages of taking bike insurance offline

- Personalised Service: Buying motorcycle insurance offline through an agent provides personalised service, where the agent can offer tailored advice and assistance based on your specific needs.

- Trust and Reliability: Some individuals may feel more secure dealing with an agent or visiting a physical office, as it provides a sense of trust and reliability.

Disadvantages of taking bike insurance offline

- Time-Consuming: The offline method can be time-consuming, requiring visits to the motorcycle insurance company’s branch and potentially waiting in long queues.

- Higher Premiums: Offline policies may come with higher premiums due to agent commissions and additional administrative costs.

- Limited Comparison: Comparing multiple policies offline can be cumbersome and less efficient, making it harder to find the best deal.

- Inconvenience: The need to physically visit the insurance office or meet with an agent can be inconvenient, especially for those with busy schedules.

Which Add-Ons Are Most Valuable? Cost-Benefit and Exclusions Explained

Understanding which add-ons offer the best value depends on your riding habits, location, and the age/value of your two-wheeler. Below is practical guidance for each major add-on:

- Zero Depreciation Cover

Best for: New bikes (up to 5 years old), high-value bikes, or if you want full claim settlement without deductions for parts.

Cost-Benefit: Raises premium by 15-20% but saves potentially thousands in depreciation deductions on replaced parts.

Common Exclusions: Limited number of claims per year; usually does not cover tyres, batteries, or mechanical breakdowns. - Engine Protect Cover

Best for: Bikes in flood-prone areas, or premium motorcycles with expensive engines.

Cost-Benefit: Small extra premium for protection against costly repairs due to water ingress or oil leaks.

Common Exclusions: Regular wear and tear, pre-existing engine issues, or damage from racing. - Roadside Assistance Cover

Best for: Daily commuters, long-distance riders, or those who travel in remote areas.

Cost-Benefit: Minimal extra cost for peace of mind in breakdowns.

Common Exclusions: Incidents in non-covered areas, repeat calls for the same issue, or non-emergency uses. - Key Protect Cover

Best for: High-tech or expensive key systems.

Cost-Benefit: Low premium, saves on costly electronic key replacement.

Common Exclusions: Lost keys due to negligence, or if entire bike is stolen. - NCB Protection Cover

Best for: Riders with a long claim-free history.

Cost-Benefit: Slightly higher premium, but preserves large NCB discounts after small claims.

Common Exclusions: Multiple claims in a year, or claims above a threshold amount. - Return to Invoice Cover

Best for: Brand-new bikes, especially financed ones.

Cost-Benefit: Higher premium, ensures full invoice value on theft/total loss.

Common Exclusions: Not available for older bikes, may not cover extra accessories.

General advice: Review the policy document for detailed exclusions. Not all add-ons are suitable for everyone—match your selection with your risk exposure and bike value. For example, a zero depreciation cover is a must for new bikes, while engine protection is vital in flood-prone states.

Common Myths and Misconceptions about motorcycle insurance in India

1. Comprehensive Insurance is Expensive

Many believe that comprehensive insurance is prohibitively expensive. While it may have a higher premium than third-party insurance, it offers extensive coverage that can help offset high costs in the event of an accident or theft.

2. Third-party insurance is Sufficient

Some think that third-party insurance is enough since it is mandatory. However, it does not cover damage to the insured vehicle, which can result in substantial out-of-pocket expenses.

3. No Claim Bonus (NCB) Applies to third-party Insurance

There is a misconception that NCB benefits apply to third-party insurance. In reality, NCB applies only to own-damage and comprehensive policies.

4. IDV is Irrelevant

The Insured Declared Value (IDV) is often misunderstood. It is crucial in determining the sum assured for one’s own damage coverage, affecting the premium and claim amount.

Frequently Asked Questions (FAQs) about motorcycle insurance in India

1. What type of insurance is mandatory for two-wheelers in India?

The law requires all two-wheeler owners to have at least third-party insurance under the Motor Vehicles Act, 1988.

2. What is the difference between third-party and comprehensive bike insurance?

Third-party insurance covers damages to others and their property, while comprehensive insurance also protects your own vehicle against theft, accidents, natural disasters, and more.

3. What is bumper-to-bumper (zero depreciation) bike insurance?

This add-on covers the full cost of replacing bike parts, excluding depreciation, ensuring higher claim payouts.

4. How is the premium for bike insurance calculated?

Premiums depend on factors like the bike’s value, engine capacity, location, rider experience, and selected coverage/add-ons.

5. Can I transfer my bike insurance when I sell my vehicle?

Yes, existing insurance can be transferred to the new owner. The buyer must notify the insurer within 14 days of purchase.

6. What are common exclusions in two-wheeler insurance policies?

Exclusions typically include regular wear and tear, riding under the influence, driving with an invalid license, and using the vehicle for illegal purposes.

7. What add-ons are available for two-wheeler insurance?

Popular add-ons include zero depreciation, engine protection, roadside assistance, and No Claim Bonus (NCB) protection.

8. How can I save on my bike insurance premium?

Opt for higher voluntary deductibles, maintain a good riding record, avoid small claims to preserve NCB, and compare policies online.

9. What documents are required to file a two-wheeler insurance claim?

You’ll need your policy document, registration certificate, FIR (if for theft/accident), and repair bills/estimates.

10. What happens if my two-wheeler insurance policy lapses?

You lose insurance coverage, risk legal penalties, and may pay higher premiums or face inspection when renewing after a lapse.

Other related articles from Bikeleague India

- Bike insurance jargons & addons in India Guide

- Bike insurance tips in India – Tips to get a lower premium

- Indian Motor Tariff (IMT) for Two-Wheelers in India

- Third party Bike Insurance Calculator – Calculate your insurance

- Bike IDV Calculator – Calculate Your Bike’s Value Online

Conclusion

Choosing the right two-wheeler insurance in India is not just a legal mandate but a critical step for your financial security and peace of mind. Understanding the differences between third-party, own-damage, comprehensive, and bumper-to-bumper plans empowers you to make an informed decision based on your needs, riding habits, and location.

Always consider valuable add-ons and review exclusions to ensure maximum coverage. Regularly compare policies, renew your insurance on time, and maintain proper documentation to avoid legal or financial hassles. By staying informed and proactive, you can protect yourself, your bike, and others on the road—making every ride safer and worry-free.

If you have any other doubts or queries about selecting and buying two-wheeler insurance in India, email us at bikeleague2017@gmail.com or share your doubts or opinions in the comments section below. We are always eager to help and assist you. Also, here are several social media accounts for Bikeleague India that should raise your suspicions.