Long story short: Two wheeler sales in India in FY 24–25 saw Hero, Honda, and TVS lead the way with strong sales. Furthermore, scooters, especially electric ones, were particularly popular. As a result, electric bike sales jumped by 21%, and brands with wide dealer networks saw the biggest wins.

India’s two-wheeler industry is closely tied to everyday life, reflecting how people move, work, and connect. As routines shift from city commutes to village errands, the industry adapts. Ultimately, behind the numbers and trends, it’s about real people making everyday choices.

Let’s see how the market performed in FY 2024–25, with a closer look at electric bike sales in India during the year. By comparing it to last year, we can see what’s changed—especially the growing interest in electric scooters and bikes. In summary, this report aims to make those changes easy to understand for everyone.

This year’s growth wasn’t just about sales—it was about people exploring new ways to get around. Not only did local demand rise, but exports also increased, and more than 1 million electric two-wheelers hit the roads. Meanwhile, scooters grew especially fast, and brands like Honda, TVS, and Suzuki attracted more riders. At the same time, Hero MotoCorp stayed a trusted name.

These shifts reflect real changes in how people travel—whether in busy cities or quiet villages. To begin, let’s start with the big picture and then look at the vehicles and brands people choose most.

Key Takeaways

- India’s two-wheeler industry made a strong comeback in FY 2024–25, growing by about 9% and almost reaching its pre-pandemic levels. This bounce-back was powered by more people choosing to buy new vehicles and a big jump in electric scooter and bike sales.

- Motorcycle sales in India FY 24–25 remained strong as scooters stole the spotlight, growing much faster than motorcycles or mopeds. Electric two-wheelers also became more common, accounting for over 6% of all two-wheelers on the road, as sales jumped by 21% in just one year.

- Most major brands saw their numbers go up, but Honda, TVS, and Suzuki grew the fastest, attracting more riders and expanding their reach. Hero MotoCorp and Bajaj maintained their strong positions, even though their growth was slightly slower.

- Exports got a healthy boost, rising by over 21%. This helped Indian manufacturers rely less on just the home market, with Bajaj and TVS especially benefiting from strong sales abroad.

- With new electric startups and international brands entering the scene—and more attention on good dealer networks and after-sales service—traditional companies are under pressure to keep improving. Being quick to adapt and innovate will decide who stays ahead.

Industry Snapshot: Fy 2024–25 Vs Fy 2023–24

To begin, we will compare FY 2024–25 with FY 2023–24, with a particular focus on electric bike sales in India FY 24–25. Following this overview, we will then turn to the details for each segment and brand, allowing for a clearer understanding of the market’s evolution. Overall, this step-by-step approach ensures that each aspect of the industry’s performance is addressed in a logical sequence.

1. Total Domestic Two‑wheeler Sales In India In Fy 24-25

According to SIAM, India’s two‑wheeler domestic sales crossed 1.96 crore units in FY 2024–25, compared to 1.80 crore in FY 2023–24.

| Metric | FY 2023–24 | FY 2024–25 | Absolute change | YoY growth |

|---|---|---|---|---|

| Total 2W domestic sales (SIAM) | 1,79,74,365 units | 1,96,07,332 units | +16,32,967 units | 9.1% |

The industry is now nearly back to its pre-COVID peak of about 2.12 crore units in FY 2018–19. Therefore, this suggests the downturn has mostly ended. With this recovery in mind, we can now examine how individual segments contributed to the overall growth. In particular, examining segment-wise performance more closely can reveal new insights into shifting consumer preferences.

2. Segment‑wise Two Wheeler Sales Performance: Scooters, Motorcycles, Mopeds In India In Fy 24-25

Scooters were the main driver of industry growth in FY 2024–25 and, as a result, had a major impact on the year’s sales figures. This shift is significant, especially when viewed alongside trends in motorcycles and mopeds. As we move forward, it becomes important to compare these segments to understand their relative contributions and future potential.

| Segment | FY 2023–24 units | FY 2024–25 units | Growth YoY |

|---|---|---|---|

| Scooters | 58,39,325 | 68,53,214 | 17.4% |

| Motorcycles | 1,16,53,237 | 1,22,52,305 | 5.1% |

| Mopeds | 4,81,803 | 5,01,813 | 4.2% |

| Total | 1,79,74,365 | 1,96,07,332 | 9.1% |

Scooters grew by nearly 17.4% year-on-year, faster than both motorcycles and mopeds. However, motorcycles had the highest sales at over 1.22 crore units, while mopeds stayed mostly stable. Taken together, these numbers illustrate the shifting preferences among Indian consumers. Clearly, each segment’s performance adds a unique dimension to the industry’s overall trajectory.

Additionally, looking at exports, two‑wheeler exports grew about 21.4% in FY 2024–25 to roughly 42 lakh units, driven by recovery in Africa and Latin America. This export revival further strengthened the industry’s overall performance. With both domestic and export markets showing resilience, the stage was set for further transformation in the sector, particularly through the rise of electric vehicles.

Electric Two‑wheelers: Clear Step‑up Vs Fy 2023–24

In FY 2024–25, electric two-wheelers moved from being a niche product to becoming a mainstream choice in India, reflecting the strong growth in electric bike sales in India FY 24–25. This transition marks a pivotal moment in the evolution of the two-wheeler sector. To illustrate this progress, it is helpful to compare recent sales figures and market share data.

- FY 2023–24: 9,48,561 electric two‑wheelers sold

- FY 2024–25: 11,49,334 units, up 21% year‑on‑year

- The share of electric vehicles within the total two-wheeler market climbed from approximately 5% to over 6%.

| Metric | FY 2023–24 | FY 2024–25 | Absolute change | YoY growth |

|---|---|---|---|---|

| Electric 2W units sold (MHI/market) | 9,48,561 units | 11,49,334 units | +2,00,773 units | 21% |

| Share of total 2W market (approx.) | ~5% | >6% | Rising | – |

According to JMK Research and media reports, electric two-wheelers make up over 50% of all EVs sold in India by volume. Key players include Ola Electric, TVS, Bajaj, and Hero. As we explore the competitive landscape, these brands stand out for their innovation and growing influence.

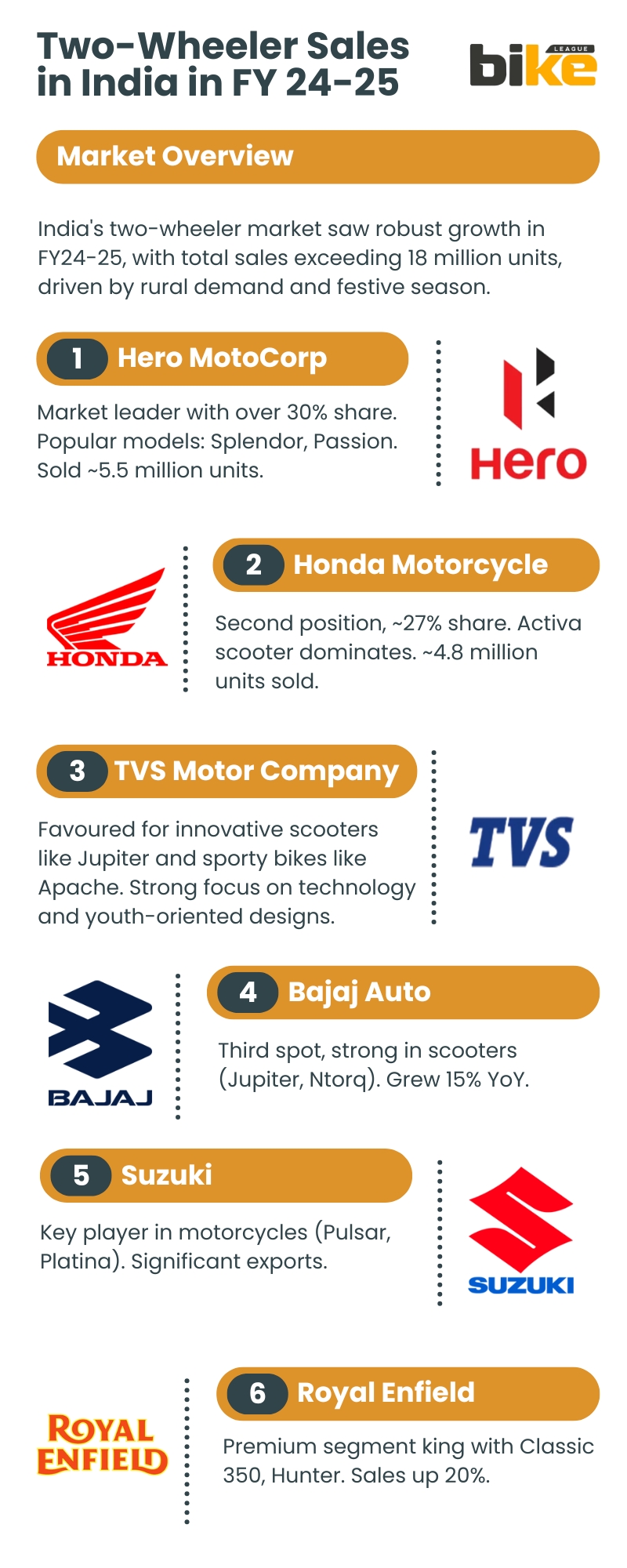

Market Share Landscape In Two Wheeler Sales In India In Fy 24-25: Who Leads?

Now, we will look at the current market share to see which companies are leading.

Retail data from FADA and industry reports show that the top four ICE companies still hold over 80% of the market.

1. Market Leadership Snapshot (retail Focus)

| Rank | Brand | FY 2024–25 Position | Trend vs FY 2023–24 |

|---|---|---|---|

| 1 | Hero MotoCorp | Largest by retail & volume | Volume up, share slightly down |

| 2 | Honda (HMSI) | Fastest major gainer | Strong share gain (~+2 p.p.) |

| 3 | TVS Motor | Steady share gainer | Gradual but consistent rise |

| 4 | Bajaj Auto | Export‑heavy major | Stable to mildly positive share |

| 5 | Suzuki Motorcycle | Fast‑growing mid‑sized OEM | Double‑digit growth |

| 6 | Royal Enfield | Niche but dominant in 250cc+ | Volume and share up in its segment |

Hero remains the market leader, but Honda, TVS, and Suzuki are quickly gaining ground, intensifying competition for market share. Against this competitive backdrop, let’s turn to a brand-wise analysis to understand what’s driving their performance.

Brand‑wise Two Wheeler Sales In India In Fy 24-25 Vs Fy 23–24

1. Top Oems – Headline Comparison

| Brand | FY 2023–24 total 2W sales | FY 2024–25 total 2W sales | Absolute change | YoY growth* |

|---|---|---|---|---|

| Hero MotoCorp | 56,21,455 units | 58,99,187 units | +2,77,732 units | 4.9% |

| Honda (HMSI) | 48,93,522 units | 58,31,104 units | +9,37,582 units | 19% |

| TVS Motor (2W only) | 38.51 lakh (3,851,000) | 43.30 lakh (4,330,000) | +4.79 lakh | 12% |

| Bajaj Auto | 37,27,923 units | 39,82,309 units | +2,54,386 units | 7% |

| Suzuki Motorcycle | 11,33,902 units | 12,56,161 units | +1,22,259 units | 11% |

| Royal Enfield | 9,12,732 units | 10,09,900 units | +97,168 units | 11% |

*YoY growth as per OEM/media disclosures based on these volumes.

All major OEMs saw growth. Notably, Honda, TVS, and Suzuki grew faster than the industry average, while Hero and Bajaj had smaller increases. This divergence underscores the importance of strategy and innovation in shaping outcomes.

2. Hero Motocorp: Still Number One, But Growing Slower Than The Market

Company remains India’s largest two-wheeler manufacturer by both volume and retail.

| Metric | FY 2023–24 | FY 2024–25 |

|---|---|---|

| Total 2W sales | 56,21,455 units | 58,99,187 units |

| Domestic sales | 54,20,532 units | 56,11,758 units |

| Exports | 2,00,923 units | 2,87,429 units |

| YoY growth (total) | – | 4.94% |

- Hero’s approximately 5% growth is still positive. However, it trails the market’s 9.1% rate, signalling a loss of some market share.

- Exports rose sharply by 43%, helping Hero diversify its business.

- Hero is still strong in 100–125cc commuter bikes like the Splendor and HF Deluxe, but faces tough competition in urban scooters and premium motorcycles.

Hero remains the leader in total sales but is growing more slowly than the market. In light of this, to maintain its lead, it needs to focus more on premium and electric models.

3. Honda Motorcycle & Scooter India (hmsi): The Big Gainer

Turning to Honda, it had the highest domestic sales growth among all major OEMs this year.

| Metric | FY 2023–24 | FY 2024–25 |

|---|---|---|

| Total 2W sales | 48,93,522 units | 58,31,104 units |

| YoY growth (total) | – | 19% |

- Honda sold over 9.3 lakh more units than last year, thanks to strong sales of Activa scooters and Shine commuter bikes.

- Retail market share is estimated to have increased by about 2 percentage points, from ~23.4% to ~25.4%.

- It also crossed 5 lakh exports in FY 2024–25, further diversifying its portfolio.

Honda’s strategies—such as launching the Activa e, showing flex-fuel technology, offering battery swapping, and expanding its BigWing premium line—have helped it lead in both growth and technology. This approach sets a benchmark for other OEMs looking to accelerate their own progress.

4. Tvs Motor: Balanced Growth And Strong Ev Credentials

TVS achieved double-digit growth in two-wheelers and is among the best-prepared brands for electric vehicles. Its focus on innovation and performance keeps it competitive.

| Metric | FY 2023–24 | FY 2024–25 |

|---|---|---|

| Total 2W sales | 38.51 lakh (3,851,000) | 43.30 lakh (4,330,000) |

| YoY growth (two‑wheelers) | – | 12% |

- TVS grew by 12%, faster than the industry average, thanks to strong sales of Jupiter and NTorq scooters, Apache motorcycles, and rural demand.

- Exports increased by about 18%, helping TVS improve its scale and profit margins.

- Sales of the TVS iQube EV jumped to 26,935 units in March 2025 alone, a 77% increase from the previous year.

In summary, TVS is steadily improving across both traditional and electric vehicles, thereby strengthening its market position. Looking ahead, its focus on innovation and diversification will likely continue to yield results.

5. Bajaj Auto: Export‑led Growth

Focusing on exports, Bajaj Auto remains India’s biggest two-wheeler exporter, sending more than 40% of its vehicles abroad.

| Metric | FY 2023–24 | FY 2024–25 |

|---|---|---|

| Total 2W sales | 37,27,923 units | 39,82,309 units |

| Domestic 2W | 22,50,585 units | 23,08,249 units |

| Export 2W | 14,77,338 units | 16,74,060 units |

| YoY growth (total) | – | 7% |

- Bajaj’s domestic sales grew by about 3%, but exports rose by around 13%, bringing total growth to 7%.

- The Pulsar and Platina models remain the mainstays of Bajaj’s motorcycle lineup, both in India and overseas.

- The Chetak electric scooter has become popular, making Bajaj one of the leading electric two-wheeler brands.

Bajaj’s focus on exports is driving its growth and helping it capitalise on strong global markets. As a result, Bajaj is better positioned to weather fluctuations in domestic demand.

6. Suzuki Motorcycle India: Fast‑growing Mid‑sized Player

Company has grown from a niche scooter maker to one of India’s top six OEMs, becoming a strong competitor in the industry.

| Metric | FY 2023–24 | FY 2024–25 |

|---|---|---|

| Total 2W sales | 11,33,902 units | 12,56,161 units |

| Domestic sales | 9,21,009 units | 10,45,662 units |

| Exports | 2,12,893 units | 2,10,499 units |

| YoY growth (total) | – | 11% |

- Suzuki’s domestic sales rose by 14%, thanks to strong demand for Access and Burgman scooters and Gixxer motorcycles.

- Exports stayed about the same, but Suzuki’s total sales are now more than twice what they were a few years ago, according to the company.

Suzuki’s strong position in urban scooters and its plans for electric vehicles are helping it continue to grow. Going forward, its ability to tap into urban and premium segments will be key to sustaining momentum.

7. Royal Enfield (eicher Motors): Premium Player, Million‑plus Scale

The company continues to lead India’s mid-size motorcycle segment.

| Metric | FY 2023–24 | FY 2024–25 |

|---|---|---|

| Total 2W sales | 9,12,732 units | 10,09,900 units |

| Domestic sales | 8,34,795 units | 9,02,757 units |

| Exports | 77,937 units | 1,07,143 units |

| YoY growth (total) | – | 11% |

- Royal Enfield now holds about 95% of the 250–350cc market, led by models like the Classic, Bullet, Hunter, and Meteor 350.

- Exports jumped by 37%, showing that Royal Enfield’s global popularity is increasing.

- New models like the Himalayan 450 and the 650cc twins are elevating Royal Enfield’s lineup to a higher level of premium.

Royal Enfield’s focus on premium models drives its high sales and keeps it ahead in the mid-size market, even though it does not target the mass segment. This strategy highlights the diversity of approaches that succeed in India’s two-wheeler landscape.

Structural Trends Behind The Numbers

1. Scooters Vs Motorcycles

Scooters grew much faster than motorcycles in FY 2024–25, making them the standout segment of the year.

| Metric | Scooters | Motorcycles |

|---|---|---|

| FY 2024–25 volume | 68.5 lakh | 122.5 lakh |

| YoY growth | 17.4% | 5.1% |

| Key beneficiaries (brands) | Honda, TVS, Suzuki | Hero, Bajaj, Honda |

Brands with strong scooter lineups, such as Honda, TVS, and Suzuki, performed better than those that focused mainly on motorcycles. This dynamic shift underscores how adapting to consumer preferences can impact market share.

2. Ev Adoption And Policy Support

Several government policies helped boost EV adoption in FY 2024–25.

| Factor | Impact on 2W market |

|---|---|

| FAME‑II & successor schemes | Lower effective EV prices, higher adoption |

| GST differential | EVs taxed lower than ICE, improving value proposition |

| Infra build‑out | More chargers/swap stations reducing range anxiety |

| OEM response | Legacy OEMs launched serious EV roadmaps and products |

As a result, electric vehicles accounted for more than 6% of all two-wheeler sales, and this share continues to grow. This momentum is likely to further shape the industry in the coming years.

3. Export Revival

At the same time, exports are once again helping Indian OEMs grow. This renewed export strength is particularly important as domestic competition intensifies.

| Brand | Export profile FY 2024–25 |

|---|---|

| Bajaj Auto | Largest 2W exporter; >40% of volumes exported |

| TVS Motor | Double‑digit export growth, strong in Africa/LatAm |

| Honda (HMSI) | Over 5 lakh units exported, ramping quickly |

| Hero MotoCorp | Exports rebounded from a low base |

With exports rising by 21.4% across the industry, OEMs can depend less on the domestic market and support higher production volumes. In this context, the export opportunity provides a valuable buffer against cyclical domestic slowdowns.

Outlook For Fy 2025–26: Tailwinds Vs Risks

Looking ahead, analysts expect this positive trend to continue into FY 2025–26, possibly pushing the industry back to its previous peak or beyond.

| Dimension | Tailwinds | Risks |

|---|---|---|

| Demand | Income growth, rural recovery, urbanisation | Rural distress, macro slowdown |

| Policy | Continued EV and localisation push | Subsidy changes, regulatory uncertainty |

| Technology | Better EVs, flex‑fuel, connectivity | Higher initial costs for new tech |

| Competition | Rich product pipelines, premiumisation | Price wars, margin pressure |

Brands that increase electric vehicle sales, expand premium product lines, and capitalise on exports are likely to perform better in the coming years. Thus, strategic agility will remain a key differentiator among OEMs.

What It Means For Stakeholders

| Stakeholder | Opportunities | Challenges |

|---|---|---|

| Consumers | Huge choice (ICE + EV, commuter to premium) | Tech complexity, resale & obsolescence worries |

| Dealers | Higher volumes, new EV‑related services | Need new skills, inventory mix management |

| Investors | Sector exiting downcycle; EV & export upside | Policy risk, high competition, cyclicality |

| Policymakers | Jobs, manufacturing scale, cleaner mobility | Balancing subsidy burden with long‑term goals |

How Dealer Networks And After‑sales Service Drove Fy 2024–25 Sales

While product launches and pricing get a lot of attention, strong distribution and after-sales service are actually more important, especially in rural and semi-urban India, where motorcycle demand is highest.

1. Dealer Expansions: Getting Closer To The Customer

In recent years, top OEMs have rapidly increased their number of outlets, and this approach continued to work well in FY 2024–25:

- Hero MotoCorp has the widest primary and secondary network in small towns and rural markets, with over 2,600 dealers and outlets across all states and territories as of early 2025. This coverage is a key reason why Hero remains the first choice in many hinterland markets and why its rural sales rebounded strongly as incomes improved.

- Honda Motorcycle & Scooter India (HMSI) has built an expansive network of 6,500+ touchpoints (RedWing, BigWing, Best Deal outlets and e: Swap stations), more than doubling its footprint over the last decade. This deep reach underpins Honda’s rapid volume gains in both scooters and motorcycles.

- Other OEMs like TVS, Bajaj, Suzuki, and Royal Enfield have also been opening more dealerships in smaller towns, not just big cities, to meet growing demand in rural and small-city areas.

1.1 Why Network Expansion Mattered More In Fy 2024–25

| Factor | Effect on FY 2024–25 sales |

|---|---|

| Rural demand recovery | OEMs with deep rural coverage captured pent‑up replacement demand |

| Improved roads & connectivity | Made two‑wheelers viable in more villages, increasing addressable market |

| Credit & financing availability | Dealer‑level tie‑ups with NBFCs/banks eased purchases |

| Proximity of showrooms & service | Reduced time/cost for buying and servicing, boosting preference |

In short, OEMs with strong networks in smaller towns were able to turn rising demand into higher sales, showing the value of early network expansion.

2. Retail Network Strength: More Than Just Outlet Count

In FY 2024–25, it wasn’t just the number of outlets that mattered, but also how they were located and targeted.

- Mass vs premium formats: For example, Hero has set up special premium outlets for models like the Xpulse 200, Xtreme 160R, and Harley-Davidson co-developed bikes, while still using its main rural network for commuter bikes.

- Honda’s RedWing network serves mass-market scooters and commuter bikes, while BigWing focuses on premium motorcycles and larger bikes.

- Honda’s Best Deal network for certified used two-wheelers gives first-time buyers a more affordable option, helping attract new customers who may later upgrade to new vehicles.

- Data shows that Hero’s 2,612 locations are particularly concentrated in large northern states such as Uttar Pradesh, Rajasthan, and Bihar, which are key markets for commuter motorcycles.

By offering a range of retail outlets, OEMs could serve both budget-conscious rural commuters and urban or premium customers, thereby boosting sales and improving the product mix in FY 2024–25.

3. After‑sales Service: The Silent Driver Of Repeat Sales

For many two-wheeler buyers, especially in rural and semi-urban areas, brand loyalty depends heavily on service availability, reliability, and overall ownership costs.

Key Levers In Fy 2024–25:

- Dense service coverage: The same networks that sell vehicles also provide regular maintenance and repairs. For people who depend on their motorcycle or scooter for work, having a nearby service centre is just as important as the product features.

- Quality and consistency: Brands like Honda and Hero run training programs for technicians and service staff to maintain high service quality across all their outlets. This helps maintain customer satisfaction and encourages word-of-mouth referrals.

- Warranty and service campaigns: Proactive recalls, free check-ups, and extended warranties help build trust. For example, Honda has had BigWing dealers reach out to customers to schedule inspections and service visits to “enhance ownership experience”.

- Spare parts availability: A wide, efficient parts network reduces repair time and keeps costs predictable, which is especially important for fleet operators, gig workers, and rural families.

3.1 How After‑sales Links To Sales Growth

| Aspect | Impact on sales outcomes |

|---|---|

| Quick & reliable service | Higher satisfaction → stronger brand loyalty → repeat purchases |

| Low running & repair costs | Better word‑of‑mouth, especially in close‑knit rural communities |

| Proactive recalls & support | Builds trust, reduces fear of new tech (e.g., EVs, fuel‑injected bikes) |

| Integrated finance + service | Easier ownership life‑cycle, boosting first‑time adoption |

Because rural India makes up about 55–65% of motorcycle sales, providing reliable service in these areas gives companies a strong competitive advantage.

4. Putting It Together: Distribution As A Competitive Moat

To sum up these points:

- Hero’s broad but traditional rural network helped it stay the volume leader, even though its growth was slower than some competitors.

- Honda, TVS and Suzuki’s aggressive network and format expansion—especially in scooters and urban/semi‑urban markets—reinforced their above‑industry growth in FY 2024–25.

- Bajaj and Royal Enfield’s targeted but strong networks in important domestic and export markets helped them perform well in their main segments.

In other words, sales results in FY 2024–25 depended not only on products and pricing, but also on which companies had the strongest dealer networks and service support as demand increased.

How Emerging Ev Startups And Foreign Players Are Shaping The Next Phase

Legacy OEMs such as Hero, Honda, TVS, Bajaj, Suzuki, and Royal Enfield still lead in total two-wheeler sales. However, new EV-focused companies and foreign brands are making a significant impact in the electric segment. This may not be clear in the overall SIAM data. Still, it is evident from the more than 1.1 million electric two-wheelers sold in FY 2024–25.

1. Ola Electric: High Growth, Then Growing Pains

Ola Electric is the most visible EV‑only player and a major driver of early adoption:

- Calendar‑year 2024: around 4.1 lakh electric two‑wheelers registered, up 52% YoY, taking >35% share of the e‑2W market that year.

- However, monthly registrations became volatile in late 2024 and 2025, with sales dipping sharply in some months amid rising competition and reported after‑sales issues.

By calendar 2025, VAHAN data indicates that TVS and Bajaj overtook Ola Electric in e‑2W sales (2,95,315 and 2,66,919 units, respectively), while Ola’s annual registrations dropped to 1,96,767 units.

This shows that a digital-first, direct-to-consumer EV brand like Ola can grow quickly. However, FY 2024–25 and CY 2025 also showed that service quality, a strong physical network, and reliable products are very important. Traditional OEMs are improving quickly in these areas.

2. Ather Energy: Premium Tech Startup Turning Scale Player

Bengaluru‑based Ather Energy has evolved from a niche premium scooter maker to a material player in the EV market:

- FY 2023–24: around 1.10 lakh units sold.

- FY 2024–25: 1,55,394 units, a 42% YoY volume increase, alongside a 29% jump in total income and improving margins.

Ather’s new family-friendly Rizta scooter, launched in FY 2024–25, quickly became its best-selling model and made up more than half of its FY 2025 sales. By late 2024, Ather had opened over 200 service centres and more than 230 experience centres, showing that even startups are now investing heavily in physical networks to support growth.

This shows that Indian engineering-focused startups, like Ather, can build strong brands and grow in the premium and family EV markets. They are also pushing the industry toward more advanced technologies, such as connectivity, fast charging, and software features.

3. Long Tail Of Ev Startups And “imported‑in‑india” Brands

Beyond Ola and Ather, there is a long tail of EV players:

Domestic startups and smaller brands offering low‑speed or affordable e‑scooters primarily for short urban commutes.

- Joint‑venture brands like Gemopai, which is a tie‑up between India’s Goreen Electric Mobility and China’s Opai Electric, are designed/manufactured in China and assembled in India.

- Numerous “local” brands that essentially re‑badge Chinese‑made vehicles, an arrangement that lowers entry barriers but can raise questions about long‑term quality, parts availability and transparency.

Analysts note that much of the lower-end electric scooter market still relies on Chinese designs, components, and, at times, complete knock-down kits (CKD). This has led to many low-priced options, but also raised concerns about:

- Fragmented after‑sales networks

- Uneven product reliability

- Unclear sourcing and localisation levels.

As government policies push for more local production and higher quality standards, some smaller or import-only brands may struggle to keep growing.

4. Chinese Oems And Other Foreign Brands: Watching, Testing, Entering

On the global side, China remains the world’s largest e‑2W market (about 6.9 million units in CY 2024). Still, it has recently seen an 8% decline in volume, prompting its big OEMs to scout for overseas growth opportunities, including India.

- Companies like Yadea, one of the largest Chinese e‑2W makers, have showcased products at Indian EV expos and publicly signalled intent to enter the Indian market with higher‑spec, long‑range scooters.

- Earlier, Chinese brand Niu had also confirmed expansion plans for India as part of its global growth strategy.

So far, fully branded Chinese OEMs have had a limited effect on India’s FY 2024–25 sales compared to local EV startups and established Indian companies. However, Chinese technology and supply chains already play a big indirect role through:

- Battery cells and key components

- Platform designs licensed or copied by Indian assemblers/startups

- Joint ventures like Gemopai that bridge Chinese manufacturing with Indian branding.

This means that foreign OEMs, especially from China, are only beginning to enter India. However, their technology, low costs, and large scale could become more important in the mass-market EV scooter segment in the next few years.

5. How Startups And Foreign Influence Change The Competitive Equation

The impact of Indian EV startups and foreign-linked brands in FY 2024–25 can be summed up as follows:

- Faster innovation cycle: Startups like Ola and Ather have pushed the envelope on range, connectivity, performance and OTA software, forcing legacy OEMs to accelerate their own EV product roadmaps.

- Price and feature pressure: Aggressive pricing by EV‑first players has compressed the window for legacy brands to overprice early EV offerings, which ultimately benefits consumers.

- Supply‑chain diversification: Heavy initial dependence on Chinese batteries and components is gradually giving way to localised packs and components, supported by PLI schemes and state incentives.

- Higher regulatory scrutiny: Quality concerns and origin‑of‑components questions have led to tighter norms on homologation, testing and subsidy eligibility—favouring players who invest in R&D and local manufacturing.

In FY 2024–25, these new and foreign-linked companies do not match Hero, Honda, or TVS in total two-wheeler sales. However, they already have a large share of the electric two-wheeler market, with over 11.5 lakh units, and are changing what people expect from Indian scooters and bikes.

Looking ahead, competition in India’s two-wheeler industry will be shaped by both established companies and a mix of traditional ICE leaders, EV-focused startups, and more active foreign OEMs and suppliers.

References

- Society of Indian Automobile Manufacturers (SIAM) – “Auto Industry Performance of March 2025 and April 2024.” Press release, 14 April 2025

- SIAM – “SIAM Releases Industry Production, Sales and Exports Figures for Q4 and FY 2023–24.” 11 April 2024

- SIAM – “Auto Industry Performance of December 2025 and Q3.” Press release, 3 December 2025

Faq About Two-wheeler Sales In India In Fy 24-25

1. How Much Did Two-wheeler Sales In India Grow In Fy 2024–25?

Two wheeler sales in India grew by about 9% in FY 2024–25. Domestic volumes increased from 1.80 crore units in FY 2023–24 to 1.96 crore units, bringing the market close to its pre-COVID peak.

2. Which Segment Grew Faster In Fy 24–25 – Scooters, Motorcycles, Or Mopeds?

Scooters grew the fastest, with sales up 17.4% year-on-year. Motorcycles grew by 5.1% and mopeds by 4.2%. Motorcycles still had the highest overall volumes.

3. How Did Electric Two-wheeler Sales Perform In Fy 2024–25?

Electric two-wheeler sales reached 11,49,334 units in FY 2024–25, up 21% from 9,48,561 units the previous year. Their share of total two wheeler sales rose from about 5% to over 6%.

4. Which Brands Led The Overall Two-wheeler Market In India In Fy 24–25?

Hero MotoCorp stayed the largest two wheeler brand by volume. Honda, TVS, and Bajaj were also among the top players. Honda, TVS, and Suzuki grew faster than the industry average.

5. How Did Hero Motocorp Perform Compared To The Overall Market?

Hero’s total two wheeler sales rose from 56,21,455 to 58,99,187 units, about 4.9% growth. This was positive, but slower than the overall market’s 9.1% growth, so Hero lost a small share of the market.

6. Why Was Honda Considered The Big Gainer In Fy 2024–25?

Honda’s total two wheeler sales rose from 48,93,522 to 58,31,104 units, a strong 19% year-on-year increase. This growth was driven by popular models like the Activa and Shine, and by a larger dealer and export network.

7. What Role Did Exports Play In India’s Two-wheeler Growth Story?

Exports grew by about 21.4% to around 42 lakh units in FY 24–25. This helped manufacturers like Bajaj and TVS expand beyond the domestic market and protected them from changes in local demand.

8. How Important Were Dealer Networks And After-sales Service In Fy 24–25?

Strong dealer and service networks were crucial, especially in rural and semi-urban areas. Brands with wide coverage, like Hero and Honda, turned recovering rural demand into higher sales and repeat purchases.

9. How Are Ev Startups And Foreign-linked Brands Changing The Two-wheeler Market?

EV-focused startups like Ola and Ather, along with Chinese-linked brands and suppliers, have sped up innovation in range, connectivity, and pricing. This has pushed established companies to improve their EVs and use more local parts.

10. What Is The Outlook For India’s Two-wheeler Industry In Fy 2025–26?

Analysts expect growth to continue, supported by income recovery, urbanisation, EV-friendly policies, and stronger exports. However, there are still risks from rural distress, subsidy changes, higher tech costs, and strong price competition.

Other Related Links From Bikeleague India

- Two wheeler Sales in India FY 2023-24 | Analysis of Top Brands

- TVS Motors Growth: Unprecedented Two-Wheeler Story FY21-25

- Top 10 bike / scooter brands as per India’s market share

- Top 10 sold petrol two-wheelers in India in FY24

- Top 10 sold petrol two-wheelers in India in FY25

Conclusion

Comparing Two wheeler sales in India in FY 24-25 with FY 2023–24 shows a clear trend:

- The industry grew by about 9%, with over 16 lakh more domestic units sold and more than 2 lakh extra electric two-wheelers added.

- All major OEMs saw growth, but Honda, TVS, and Suzuki grew faster than the market. At the same time, Hero and Bajaj had more modest but still positive results.

- Royal Enfield sold over a million units and strengthened its lead in the mid-size motorcycle segment.

Comparing FY 2024–25 with FY 2023–24 shows that India’s two-wheeler sector is recovering and changing quickly. Strong domestic demand, more electric vehicle sales, and higher exports have all helped the industry grow again. While established brands like Hero still lead in total sales, companies like Honda, TVS, and Suzuki are gaining market share quickly through new products and expanding their networks.

The rise of electric startups and international brands is intensifying competition and driving greater innovation. In the future, success in India’s two-wheeler market will depend on adopting new technology, serving premium and urban customers, and building strong export and after-sales networks. Companies that adapt quickly to these trends will be best placed to succeed.

If you have more questions about Two wheeler sales growth in India in FY 24-25, you can email us at bikeleague2017@gmail.com or leave a comment below. We are always happy to help. You can also find Bikeleague India on social media.