Long story short: Learn about the top-selling electric two-wheelers in India in FY26, model-wise. See which models dominated EV sales with the reasons behind their popularity.

FY26 was a big year for electric two-wheelers in India. Between April 2025 and March 2026, 14,01,818 units were sold—a huge jump of nearly 22% from the year before. Electric two-wheelers now make up over half of all EV sales in the country, showing just how quickly people are making the switch. They also grabbed a slightly bigger share of the overall two-wheeler market, moving up to 6.54% from 6.09% last year.

The electric two-wheeler scene in FY26 was full of surprises. TVS Motor Company overtook Ola Electric to become number one for the first time, while Ola’s sales took a big hit, dropping by more than half after being last year’s leader. Meanwhile, brands like Ather Energy, Hero MotoCorp’s Vida, and River Mobility grew at record speeds. In this article, we’ll break down the top 10 best-selling electric two-wheelers of FY26, chat about what made them so popular, and see what these trends might mean for the future.

Key Takeaways

- TVS Motor Company led the pack in FY26, selling a whopping 3,41,513 electric two-wheelers. That’s the first time any Indian manufacturer has crossed the 3 lakh mark in just one year! The iQube and the new Orbiter were the main stars.

- Ola Electric faced a tough year, with sales dropping by more than half—from 3,44,009 units in FY25 to just 1,64,295 in FY26. Most of the trouble came from ongoing service and quality problems that frustrated a lot of customers.

- Ather Energy had its best year yet, growing an impressive 82.34% and selling 2,39,124 scooters. Most of this success was thanks to the Rizta family scooter, which made up about 70% of all Ather sales.

- Hero MotoCorp’s Vida brand really stole the show, jumping 196.13% to 1,44,330 units—mainly because of the new Vida VX2 series launched in July 2025.

- When the PM E-DRIVE subsidy was set to end on March 31, 2026, everyone rushed to buy. March 2026 saw a record 1,90,941 units sold—the biggest single month in India’s electric two-wheeler history!

- The big four—TVS, Bajaj, Ather, and Ola—held about 80% of the market, showing that established players are now leading the charge instead of startups.

- River Mobility grew the fastest of all, with a massive 426.35% jump—thanks to the River Indie scooter. Clearly, more people want affordable, practical electric rides.

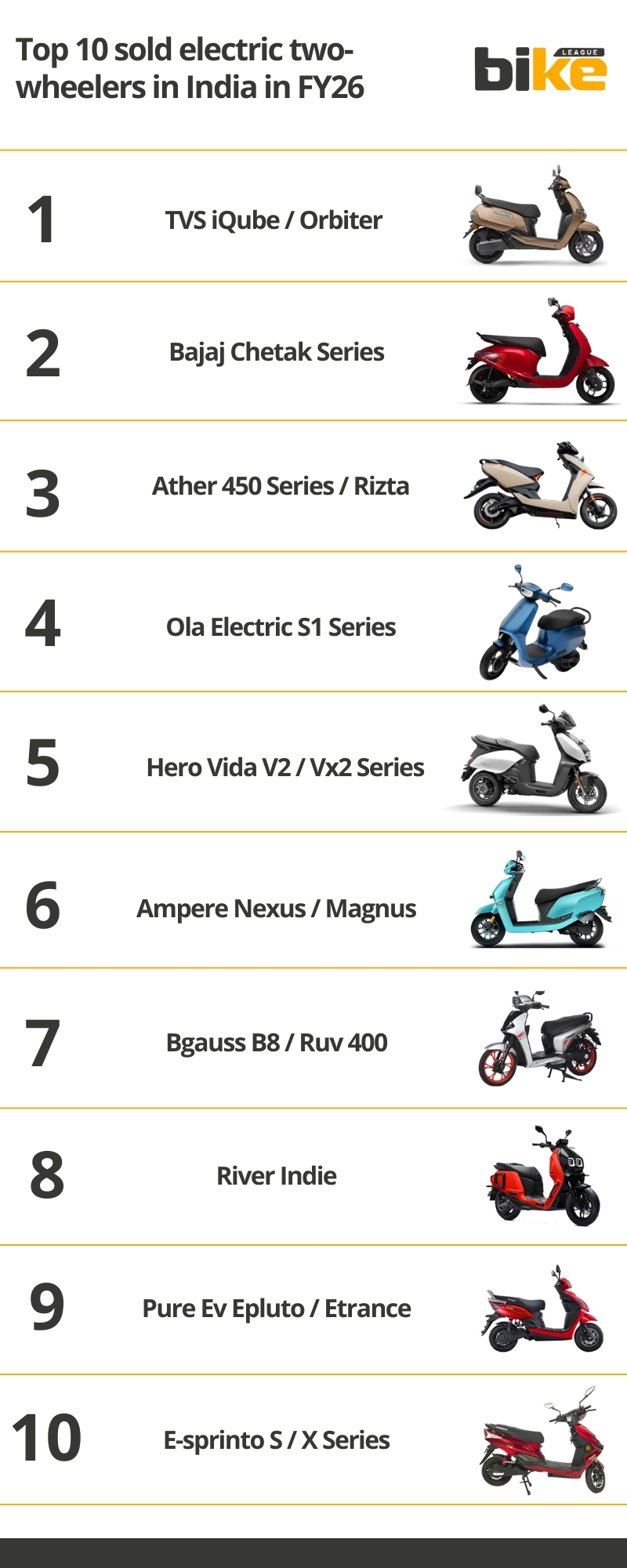

Top 10 Sold Electric Two-wheelers In India In Fy26

| Rank (FY26) | Model | FY25 Sales | FY26 Sales | Volume Change | Growth vs FY25 |

|---|---|---|---|---|---|

| 1 | TVS iQube / Orbiter | 2,37,929 | 3,41,513 | +1,03,584 | +43.54% |

| 2 | Bajaj Chetak Series | 2,30,806 | 2,89,349 | +58,543 | +25.34% |

| 3 | Ather 450 / Rizta | 1,31,173 | 2,39,124 | +1,07,951 | +82.34% |

| 4 | Ola Electric S1 Series | 3,44,009 | 1,64,295 | -1,79,714 | -52.28% |

| 5 | Hero Vida V2 / VX2 | 48,738 | 1,44,330 | +95,592 | +196.13% |

| 6 | Ampere Series | 40,169 | 61,563 | +21,394 | +53.26% |

| 7 | BGauss B8 / RUV 400 | 17,343 | 26,201 | +8,858 | +51.08% |

| 8 | River Indie | 4,247 | 22,354 | +18,107 | +426.35% |

| 9 | Pure EV Epluto / Etrance | 8,982 | 14,352 | +5,370 | +59.79% |

| 10 | E-Sprinto S / X Series | 1,409 | 12,582 | +11,173 | +792.97% |

Source: VAHAN Portal / FADA FY 2025–26

Model-wise Information About The Top 10 Electric Two-wheelers In India In Fy26

1. Tvs Iqube / Orbiter

- FY26 Sales: 3,41,513 units

- FY25 Sales: 2,37,929 units

- Growth: +43.54%

TVS Motor Company made history in FY26 by becoming the first Indian manufacturer to cross the 3 lakh unit milestone in a single fiscal year for electric two-wheelers — and by dislodging Ola Electric from the top spot for the very first time. The iQube remained the primary volume driver, with the newer Orbiter platform (launched August 2025) steadily adding incremental sales. TVS’s average monthly sales in FY26 were around 28,000 units, with peaks of 34,800 units in January 2026 and a record 49,719 units in March 2026.

TVS’s dominance stemmed from a multi-pronged strategy: aggressive pricing of the iQube 2.2 kWh variant to compete with petrol scooters, rapid expansion of the dealer network beyond 950 touchpoints, and the launch of Battery-as-a-Service (BaaS) across the iQube range in March 2026, which substantially lowered the entry price. Additionally, the iQube’s range of variants from ₹90,000 to ₹1.80 lakh gives it coverage across the mass and premium-mass segments that no rival can match. Heritage in the Jupiter and Apache has also built a deep reservoir of trust in tier-2 and tier-3 markets, now being actively leveraged for EV sales.

Model Links

2. Bajaj Chetak Series

- FY26 Sales: 2,89,349 units

- FY25 Sales: 1,31,173 units

- Growth: +82.34%

Bajaj Auto retained second position in FY26, with the Chetak crossing the 2.89 lakh mark — its best-ever fiscal year performance. The brand had to navigate a difficult patch in August 2025, when production dipped to around 12,000 units due to a shortage of rare earth magnets for motors. However, once supply normalised in September, Bajaj bounced back strongly, and the launch of the Chetak 30 Series (June 2025) and the ultra-affordable Chetak C2501 (January 2026, priced below ₹1 lakh) gave the range fresh momentum.

March 2026 was Bajaj’s best-ever month with 46,544 Chetaks delivered — second only to the post-DRIVE subsidy panic-buying surge. Bajaj’s story is compelling for its deliberate avoidance of deep discounting. Instead, the Chetak sells on the strength of its premium retro build quality, 153km real-world range (35 Series), Bajaj’s 4,000-point service network across 800 cities, and its status as a true household name in India. While the gap between Bajaj and TVS remained significant, it narrowed considerably throughout the year.

Model Links

3. Ather 450 Series / Rizta

- FY26 Sales: 2,39,124 units

- FY25 Sales: 1,31,173 units

- Growth: +82.34%

Ather Energy delivered a spectacular FY26, surpassing 2 lakh units for the first time in a fiscal year and posting 82.34% growth — the highest among all major OEMs. Approximately 70% of all sales came from the Ather Rizta family scooter, cementing its status as one of India’s favourite electric scooters. October 2025 marked the first time monthly sales crossed the 20,000-unit mark, and the fiscal closed with a stunning record of 35,688 units in March 2026.

Ather’s strategic pivot from a premium performance brand to a “family mobility” brand — through the Rizta — unlocked a far larger addressable market. The Rizta’s combination of the largest seat in India, a 34-litre boot, 159km IDC range, and OTA updates at a BaaS-linked price of around ₹76,000 made it genuinely competitive with petrol scooters on total cost of ownership. The 450 series (450X, 450S, 450 Apex) continued to serve performance-oriented buyers, sustaining Ather’s brand equity at the premium end. To support future scale, Ather is building a massive new manufacturing facility at Aurangabad (AURIC), which will expand capacity from 4.2 lakh to 14.2 lakh units annually.

Model Links

4. Ola Electric S1 Series

- FY26 Sales: 1,64,295 units

- FY24 Sales: 48,738 units

- Growth: -52.28%

Ola Electric’s FY26 was, without question, the biggest decline story in Indian EV history. The company, which was the market leader in FY25 with nearly 3.44 lakh units and a 29.93% market share, slid to fourth place in FY26 with just 1.64 lakh units and a market share of around 11.7%. Monthly sales, once averaging over 30,000 units for much of FY25, collapsed into four-figure territory from November 2025 onwards — with just 7,512 units sold in January 2026 and 4,000 in February 2026.

The root cause was a combination of well-documented product quality issues, after-sales service failures (spare parts shortages, long repair wait times), and a loss of consumer trust that was amplified on social media. A regulatory inquiry from the Ministry of Heavy Industries into discrepancies between Ola’s reported sales and VAHAN portal data added to the reputational damage. Ola’s post-IPO scrutiny on the stock market also intensified the pressure. The company ended FY26 ranked 5 in the monthly charts (briefly dropping to No. 6 in February 2026, behind Greaves), before recovering to 10,117 units in March 2026. Bhavish Aggarwal acknowledged these challenges publicly, and Ola claims over 80% of vehicles are now serviced on the same day. Whether the remediation is enough will define Ola’s FY27.

Model Links

5. Hero Vida V2 / Vx2 Series

- FY26 Sales: 1,44,330 units

- FY25 Sales: 48,738 units

- Growth: +196.13%

Hero MotoCorp’s Vida brand was the breakout performer in FY26, with a 300% growth rate, tripling volumes to 1.44 lakh units. The transformative product was the Vida VX2 series, launched in July 2025, offering a removable battery architecture, a BaaS model at ₹44,990 with a subscription charge of ₹0.96/km, and a price point that made high-speed EVs genuinely accessible to first-time buyers. Volumes scaled from 6,500 units in April 2025 to over 12,500 units by February 2026, with a record 21,434 units in March 2026 — an 11% share, the brand’s highest ever in a single month.

What gave Vida an outsized advantage over pure-play EV startups is Hero MotoCorp’s unrivalled reach — the world’s largest two-wheeler manufacturer by volume, with dealer presence across every corner of India including the smallest towns. Hero also has approximately 2,500 charging points in partnership with Ather Energy. The February 2026 launch of the Vida VX2 Plus KKR (Knight Edition Evooter), as the title partner of the Kolkata Knight Riders in IPL 2026, gave the brand a strong aspirational appeal among urban youth.

Model Links

- Hero Vida V2

- Vida VX2

- Vida V2 Pro

- Vida VX2 Plus (KKR Knight Edition)

6. Ampere Nexus / Magnus

- FY26 Sales: 61,563 units

- FY25 Sales: 40,169 units

- Growth: +53.26%

Greaves Electric Mobility, which markets the Ampere brand, had a strong FY26, with 53.26% growth and over 61,500 units sold. Targeting the budget and mid-range scooter segment, the Ampere brand has built steady traction in tier-2 and tier-3 cities. February 2026 marked the most notable moment of the year, when Greaves Electric overtook Ola Electric in monthly sales for the first time — a symbolic milestone reflecting just how far Ola had fallen and how far Greaves had risen. With its expanding dealer network and competitive pricing, Greaves is positioned to cross the 80,000-unit mark in FY27.

Model Links

7. Bgauss B8 / Ruv 400

- FY26 Sales: 26,201 units

- FY25 Sales: 17,343 units

- Growth: +51.08%

BGauss, the EV brand from RR Kabel, posted a healthy 51.08% growth in FY26, crossing the 26,000-unit milestone for the first time. Both the B8 and RUV 400 continue to appeal to buyers who value build quality and feature richness in the mid-segment. Although BGauss does not have the marketing firepower of the top-four OEMs, its word-of-mouth reputation for reliability is earning it consistent repeat and referral buyers. Expanding the service network in major metros will be critical for BGauss to push further into the 40,000+ unit bracket.

Model Link

- BGauss B8

- BGauss RUV 400

8. River Indie

- FY26 Sales: 22,354 units

- FY25 Sales: 4,247 units

- Growth: +426.35%

River Mobility’s River Indie was, without doubt, FY26’s most exciting newcomer story. After growing 426.35% off a small base, the Indie demonstrated a strong market for well-built, quirky, practical electric scooters with high storage volume. In particular, the Indie features a massive 40-litre underseat storage — the largest of any scooter in India — is priced around ₹1.25 lakh, and combines retro-modern design with connected features. River’s challenge now is ramping up production fast enough to meet growing demand, and expanding its service presence beyond the metros where it currently operates.

9. Pure Ev Epluto / Etrance

- FY26 Sales: 14,352 units

- FY25 Sales: 8,982 units

- Growth: +59.79%

Pure EV crossed the 14,000-unit mark in FY26, posting a 59.79% growth. Targeting the sub-₹1 lakh electric scooter space, the brand focuses on affordability as a key purchase driver. The EPluto 7G continues to be its steady volume contributor, while the ETrance Neo addresses the premium-affordable segment. As entry-level electric scooters become increasingly important with the market’s shift toward mainstream adoption, Pure EV is well-positioned to scale further, provided it continues to strengthen its service infrastructure in the cities where it sells.

Model Links

- Pure EV EPluto 7G

- Pure EV ETrance Neo

- Pure EV ETrance+

10. E-sprinto S / X Series

- FY26 Sales: 12,582 units

- FY25 Sales: 1,409 units

- Growth: +792.97%

E-Sprinto Green Energy recorded the highest growth rate of any brand in FY26’s top 10, with a staggering 792.97% jump — growing from 1,409 units in FY25 to 12,582 units in FY26. Although the base was very small, this kind of exponential growth indicates a brand finding its footing rapidly. Focusing on the mass-market end of the electric scooter segment, E-Sprinto targets daily commuters with affordable, reliable models. Sustaining this growth in FY27 will require scaling service capabilities and expanding from current city concentrations to a national presence.

Model Links

- E-Sprinto S series

- E-Sprinto X series

What Are The Reasons For The Growth Of Vida In India In Fy26?

Hero Vida’s jump in FY26 was mainly driven by the VX2 launch, BaaS pricing, and Hero’s distribution strength. More affordable pricing from the VX2 helped the brand reach buyers who were previously out of its price range.

1. Product Reset

The Vida VX2 series, launched in July 2025, was the largest product driver of growth. It brought a more mass-market positioning, and Autocar Pro notes that the BaaS-linked pricing made the scooter far more accessible to first-time EV buyers.

2. Pricing Advantage

Battery-as-a-Service sharply lowered the upfront purchase price and improved the value equation. That mattered a lot in India because many buyers compare EVs directly with petrol scooters, focusing on entry and running costs.

3. Network And Trust

Hero’s huge dealer and service network gave Vida a trust advantage that pure EV startups could not easily match. Buyers in smaller cities tend to value after-sales support heavily, and Hero’s reach helped the brand convert that confidence into sales.

4. Charging Support

Vida also benefited from its own charging ecosystem. Earlier reports show that Hero Vida is setting up fast-charging points in multiple cities, reducing range anxiety and improving the ownership story for urban users.

5. Mainstream Appeal

The brand’s shift toward a more practical, family-friendly scooter appeal also helped. Instead of targeting only early adopters, Vida started fitting the needs of ordinary Indian scooter buyers who want a reliable, easy-to-own electric option.

What Are The Reasons Behind The Dip In Sales Of The Ola S1 Series In India In Fy26?

Ola Electric’s S1 series fell because service problems, product reliability issues, and trust erosion started outweighing the brand’s early hype. As competitors like TVS, Bajaj, Ather, and Hero Vida improved their products and support networks, many buyers shifted away from Ola.

1. Service Issues

The biggest complaint was after-sales service, with owners reporting long repair waits, spare-parts shortages, and weak issue resolution. Ola’s own leadership later acknowledged that service challenges hurt brand trust and sales.

2. Product Problems

Users also reported technical glitches, hardware issues, and durability concerns, which made the scooters feel risky to many buyers. In a maturing EV market, that kind of ownership pain can quickly turn into lost sales.

3. Trust Loss

Ola built huge early demand through hype, but repeated customer complaints damaged confidence over time. Once trust in a two-wheeler brand drops, buyers tend to move toward more established names with stronger reputations for support.

4. Market Pressure

Competition also became much tougher, with TVS, Bajaj, Ather, and Hero Vida offering better service reach, more reliable products, and stronger value propositions. Ola lost share as those brands scaled up and gave customers better alternatives.

5. Business Strain

Ola also faced regulatory scrutiny, falling revenue, and sharp sales declines, which added pressure to the brand’s image. The result was a full slowdown rather than just a temporary dip.

What Factors Drove The Growth Of Electric Two-wheelers In India In Fy26?

Several key factors shaped the electric two-wheeler segment’s performance in FY26:

- PM E-DRIVE Subsidy Deadline Effect: The government’s PM E-DRIVE scheme, which offered up to ₹10,000 per vehicle, was scheduled to end on March 31, 2026. This created a massive pull-forward demand, with March 2026 recording 1,90,941 units — the single highest monthly figure ever in India’s e2W history. Six-figure monthly sales were achieved in 10 of 12 months in FY26, compared to just four months in FY25.

- Iran Oil Crisis Impact: The geopolitical crisis involving Iran in the second half of FY26 pushed petrol prices above ₹110/litre in multiple cities. This significantly strengthened the total cost of ownership (TCO) argument for electric scooters, accelerating fence-sitter conversions in urban and semi-urban markets.

- Legacy OEM Consolidation: The top four OEMs — TVS, Bajaj, Ather, and Hero — collectively held about 80% of the market. Their scale advantages in manufacturing, deep dealer networks, established service infrastructure, and consumer trust proved decisive against EV startups.

- GST Reduction (September 2025): The government reduced GST on electric vehicles in September 2025. While this narrowed the price gap between EVs and ICE scooters and slightly moderated the relative cost advantage, it also made electric scooters available at previously unattainable price points — opening the market to new buyers.

- Battery-as-a-Service (BaaS) Adoption: Multiple OEMs — TVS, Ather, Hero Vida, and Greaves — introduced or expanded BaaS models, decoupling the battery cost from vehicle ownership and dramatically lowering the upfront purchase price. This made premium EVs accessible to first-time buyers.

- Family Scooter Positioning: The success of the Ather Rizta, Hero Vida VX2, and TVS iQube demonstrated that buyers are increasingly choosing EVs for family use — not just as a secondary or commuter vehicle. Models with large storage, comfortable seating, and connected features resonated strongly.

- Gig Economy and Commercial Demand: Rising demand from e-commerce and food delivery fleets for last-mile vehicles continued to add a structural demand base beyond retail buyers.

- New Entrants and Competitive Pressure: Japanese OEMs — Honda, Yamaha, and Suzuki — entered or significantly expanded in the e2W space in FY26, raising the bar on refinement and reliability and validating the segment’s long-term potential.

How Did Market Trends In Fy26 Impact The Electric Two-wheeler Segment?

- TVS Becomes Undisputed Leader: For the first time, TVS Motor Company led both the monthly and full-year EV charts — a crown it had never held before. Its BaaS strategy, Orbiter launch, and network depth created a durable advantage.

- Ola’s Historic Collapse: The 52% decline in Ola Electric’s sales is one of the sharpest brand collapses in Indian automotive history. It underscored that in a maturing EV market, after-sales service quality and brand trust matter as much as product innovation.

- Ather’s Rise to Third: Ather Energy’s ascent to the No. 3 position, ahead of Ola, was a defining moment. The Bengaluru-based startup demonstrated that with the right product pivot (Rizta for families), a premium brand can scale aggressively and enter the mass market.

- Hero Vida’s Surprising Acceleration: A 196% growth rate for Vida surprised even industry analysts. It validated the hypothesis that when a truly mass-market player like Hero backs an EV brand with the right product and a vast distribution network, volumes can ramp up exponentially fast.

- Market Penetration Still Low: Despite record volumes, e2W penetration was only 6.54% of total two-wheeler sales in FY26. With over 93% of buyers still choosing petrol two-wheelers, the long-term growth runway remains enormous.

- Consolidation of the Competitive Landscape: The top 10 OEMs together held 94% of the market, with smaller players struggling to scale. The era of multiple EV startups competing for share is giving way to a few well-funded, well-distributed players dominating.

- Electric Motorcycles Remain Marginal: Ola’s Roadster X was the only notable electric motorcycle launched in FY26. The e2W market remains overwhelmingly scooter-dominated, with electric motorcycles accounting for less than 2% of segment volumes.

- River and E-Sprinto Signal a Long Tail: Despite the consolidation at the top, the emergence of River Mobility and E-Sprinto in the top 10 shows that focused, well-executed product strategies can still carve out a meaningful niche even against much larger OEMs.

Other Related Links From Bikeleague India

- Top 10 sold petrol two-wheelers in India in FY26

- Top 10 Sold Electric Two-Wheelers in India in FY25

- Top 10 sold petrol two-wheelers in India in FY24

- Vida v2 Plus

- Vida V2 Pro

Conclusion

FY26 marked a major shift for India’s electric two-wheeler market. For the first time, sales crossed 14 lakh units, proving that strong growth can happen even as government subsidies decline and price gaps with petrol vehicles narrow. Additionally, the year showed how established brands used their wide networks, strong reputations, and reliable service to beat early leaders. TVS, Bajaj, Ather, and Hero all set new records, while Ola’s sharp drop highlighted the risks of letting service quality slip.

As we move into FY27, most subsidies will be gone, and Japanese brands are entering the market in a big way. The next group of EV buyers, mainly everyday commuters, will look for even better reliability, resale value, and support. Brands that provide quality products, strong service across India, and fair prices will drive the next stage of electric two-wheeler growth in the country.

We hope this overview gave you a clear picture of the top 10 electric two-wheelers sold in India in FY26. If you have any questions or want more information, feel free to leave a comment or reach out to us. Stay tuned to Bikeleague India for the latest updates on the two-wheeler market.